Construction Loan for a Rental Property: How to Get One

Learn how a construction loan for a rental property work, what lenders require in 2026, costs, and step-by-step how to qualify and reach first draw. Understand the DSCR financing exit strategy.

CONSTRUCTION LOANS

Nick Thomas

6/12/20269 min read

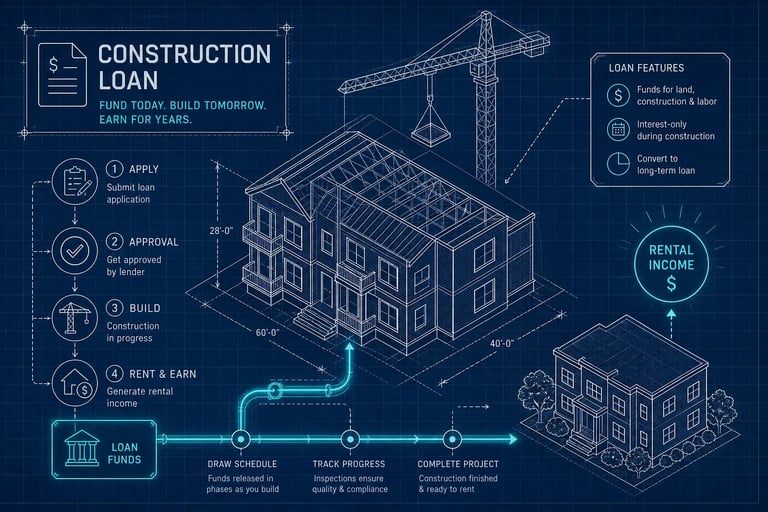

Yes, you can get a construction loan for a rental property. But the process works differently than anything you've encountered with a standard mortgage, and walking into it without understanding the rules will cost you months of wasted time and real money. Investors building single-family rentals, small multifamily projects, or full build-to-rent communities face a completely separate underwriting world from owner-occupied borrowers, different loan structures, different approval criteria, and a funding timeline that moves in draws rather than lump sums.

The good news: once you understand how investment construction financing actually works, it's far more accessible than most investors assume. Private portfolio lenders structure these programs specifically for rental investors and builders, which means the underwriting is designed around your project and exit strategy rather than your W-2. This article breaks down the loan types available, what lenders actually look for, what it's going to cost you in 2026, and exactly how to get from application to first draw.

Can I Get a Construction Loan for a Rental Property? What Lenders Look For

The first thing to understand is that investor construction loans live in a completely different lane from owner-occupied programs. FHA construction loans are not available for investment properties, period. If you try to use a standard owner-occupant construction product for a rental build, you'll hit a wall fast. Investors must go through private lenders, portfolio lenders, or non-bank lenders, and that is not a disadvantage. It's just a different set of rules, and knowing them upfront eliminates dead ends before they waste your time.

During the construction phase, lenders don't underwrite your loan based on current property income because the property doesn't exist yet. Instead, they use a loan-to-cost (LTC) framework, sizing the loan against your total project cost and the projected as-completed value. Cost control, project completability, and the strength of your exit plan drive the approval decision at this stage. Projected rent matters too, but it enters the picture primarily when the lender evaluates whether your takeout financing will work once the property is stabilized and leased.

How Investor Construction Loan Qualification Actually Works

Investor construction loan underwriting has three distinct layers: borrower strength, project viability, and exit strategy. Lenders evaluate all three, but each carries different weight depending on the stage of the loan.

Credit score, down payment, and cash reserve requirements

For investment property construction loans, most lenders set a credit score baseline of 680, with better pricing and terms available at 700-720 and above. A small number of niche programs may accept 660 in select scenarios, but 680 is the more common floor. Down payment requirements run 20%-25% at minimum for investment projects, and some programs require more depending on project scale and lender type. Cash reserves and contingency funds, typically 5%-10% of the total build cost, are standard because lenders need confidence that you can absorb cost overruns without defaulting mid-project. If you're approaching a lender without adequate reserves, that's the first thing to fix before submitting an application.

How projected rent and pro forma NOI factor into approval

Lenders underwriting rental construction loans want to see that your exit strategy works, not just that the build plan is sound. Most lenders run a conservative stabilized cash flow analysis on the completed property to confirm it can support permanent financing. The standard approach: an independent appraiser estimates market rent for comparable completed properties in the area, and lenders commonly qualify at 75% of that gross estimated rent to account for vacancy and maintenance, a convention aligned with standard rental property underwriting practice. If the pro forma DSCR doesn't pencil at stabilization, the construction loan approval becomes significantly harder regardless of how strong your credit profile is.

Why builder experience and project documentation carry serious weight

Lenders treat inexperienced sponsors as completion risk, and they price it accordingly. A borrower who has developed 15-20 properties represents a fundamentally different risk profile than someone attempting their first ground-up project. Many lenders directly tie leverage to experience, less experience typically means a lower LTC or stricter reserve requirements.

Before you contact any lender, have your documentation organized: detailed construction plans, a vetted licensed contractor with a verifiable track record, a project budget broken down by line item, a realistic build timeline, and documentation of any existing real estate holdings. Showing up to the underwriting table without these materials delays the process by weeks.

The Three Loan Structures Built for Build-to-Rent Projects

Not all investor construction loans are structured the same way, and choosing the wrong structure can mean paying closing costs twice or losing flexibility you'll want later. For a deeper dive into specific lending programs for ground-up work, see our guide to Ground-Up Construction Loans for Real Estate Investors | Cape Henry Capital.

One-time-close construction-to-permanent loan

This structure combines the construction phase and permanent mortgage into a single loan with one closing. The lender releases funds in draws as construction milestones are hit, you make interest-only payments on the drawn balance during the build phase (typically 12-18 months), and the loan automatically converts to long-term permanent financing when the project is complete. The core advantage is straightforward: one set of closing costs, no second qualification required at conversion. Because the permanent loan terms are set at the start, you're also protected against rate movement during the build. For additional background on how one-time-close programs work in practice, review the explanation of one-time-close construction loans.

Construction-only loan with a DSCR takeout

Some investors prefer to keep construction and long-term financing completely separate. A construction-only loan funds the build. Once the property is complete and leased, the investor refinances into a DSCR rental loan on their own timeline. This approach gives maximum flexibility to shop permanent financing terms after construction, but it means qualifying twice and paying two full sets of closing costs. It's a strong fit for investors who want to optimize their long-term rental loan independently or who anticipate significant equity at completion that they want to capture through aggressive DSCR refinance terms.

Build-to-rent specialized programs

Build-to-rent (BTR) is not a single standardized loan product. Some lenders structure it as a single-close construction program with a defined rental hold strategy built into the loan terms from the beginning. Others structure it as construction debt followed by a DSCR refinance at stabilization. What distinguishes BTR programs from generic construction loans is that they're designed explicitly for properties intended to generate rental income. Some private lenders factor projected rent into underwriting more heavily than conventional lenders, incorporating higher LTC ratios or more favorable DSCR assumptions for investors who can demonstrate strong market rent data, which can improve leverage and approval outcomes for well-prepared borrowers. For an industry perspective on how underwriters treat BTR projects, see this discussion of how lenders underwrite build-to-rent loans.

Rates, Fees, and Draw Schedules to Plan for in 2026

Construction loans for investment properties cost more than conventional mortgages. Investors who model their project using conventional mortgage rates will end up with inaccurate carry cost projections, plan for the real numbers from the start.

Where construction loan interest rates land right now

In 2026, construction loans for investment properties are generally pricing 1-2 percentage points above conventional mortgage rates, putting most investors in the 8%-13% range depending on credit profile, leverage, lender type, and project scale. These ranges reflect current private lender market conditions and should be treated as illustrative, always confirm current pricing directly with your lender. Rates during construction are often variable; the permanent loan rate is either locked at the initial closing (for one-time-close structures) or set when the takeout loan is originated (for construction-only). Model your carrying costs using the higher end of this range. If you budget at 8% and your actual rate comes in at 11%, the difference over a 12-month construction period on a $500,000 loan is roughly $15,000 in unplanned interest expense.

How the draw schedule and inspection fees add up

Construction funds are released in milestones, not in a lump sum at closing. Most residential construction projects involve 4-6 draws, with an independent inspector verifying completion of each phase before the lender releases the next tranche of funds. Inspection fees typically run $150-$600 per visit depending on the lender and project complexity. Origination fees for construction loans generally land at 1%-2% of the loan amount. Appraisals for ground-up projects cost $800-$1,500, and full title and closing costs commonly add another $3,000-$5,000 or more to the project budget. None of these are surprises if you budget for them in advance.

Budgeting for conversion or permanent financing costs

Investors using a construction-only structure will face a second full set of closing costs when they refinance into a DSCR or other permanent rental loan at stabilization. Even in a one-time-close structure, confirm with the lender exactly what, if anything, they charge at the conversion point. For a realistic all-in cost estimate on a $500,000 construction project, your budget should include build costs, origination, inspection fees, appraisal, title, interest carry during construction, and permanent loan closing costs as a separate line item. Investors who undercount financing costs on the front end often find themselves short at a critical project stage. For authoritative guidance on originating and underwriting construction-to-permanent financing, consult Fannie Mae's construction-to-permanent financing FAQs.

How Cape Henry Capital Structures Construction Loans for Rental Investors

Cape Henry Capital's construction financing programs are built for real estate investors and builders, not owner-occupants. That distinction matters because it means underwriting is structured around the investment, the project, and the exit strategy rather than around a borrower's W-2 income or personal tax returns.

Single-lot builds, multi-unit projects, and full developments

Cape Henry Capital works across a range of project types: single-lot builds for individual rental properties, multi-unit projects for investors developing small apartment buildings or townhome clusters, and larger build-to-rent developments. The programs are designed to cover ground-up construction financing for rental investors, giving borrowers a consistent lending relationship from project start through completed structure rather than having to source multiple lenders at different stages.

The draw-to-DSCR path for buy-and-hold investors

For buy-and-hold and BRRRR-style investors, a construction-to-DSCR path is a natural fit. Investors use construction financing to build the property, then transition into a DSCR rental loan once the project is complete and leased. The DSCR loan qualifies based on property cash flow rather than personal income, which means self-employed investors and those with complex tax returns aren't penalized at the refinance stage. For investors whose goal is to build rental assets from the ground up and hold them long-term, this two-step path removes the income verification friction that would otherwise limit their ability to scale. Cape Henry Capital structures this path for qualifying borrowers, contact their team directly for current program terms.

Getting pre-qualified and moving to the underwriting table

For investors who have found a lot or have a project ready to move on, working with a lender who can turn around a pre-qualification quickly compresses the evaluation timeline significantly compared to bank-based construction programs. Cape Henry Capital is built to move at the pace investors need, reach out at capehenrycapital.com to get a no-obligation quote and discuss your project with a decision-maker directly. If you're still evaluating which financing product fits your strategy, you may find our overview on Rental Property Loans: Which Type Fits Your Strategy? | Cape Henry Capital helpful when comparing long-term hold options.

The Step-by-Step Path From Application to First Draw

Documents and prep work before you apply

Getting organized before you contact a lender compresses the approval timeline by weeks. The core documents you need include:

A detailed construction budget with line-item cost breakdown and project plans

A licensed contractor with a verifiable track record and signed contract

Evidence of land ownership or a land purchase agreement

Proof of down payment funds and cash reserves

Documentation of existing real estate holdings or relevant development experience

Exit strategy support: projected rent, market comparables, and stabilization timeline

Private lenders require fewer documents than banks, but they still need enough to verify the borrower, underwrite the project, and confirm how the loan will be repaid. Showing up with incomplete materials doesn't slow the lender down, it slows you down.

What the approval and closing timeline looks like

A realistic construction loan timeline with an organized private lender breaks down like this: pre-qualification in days 1-3, document submission and underwriting review from days 4-15, appraisal and title work from days 10-20, and approval and closing around days 20-30. The first draw is released upon verified construction start. Construction phases typically run 6-12 months from first draw to completion, with funds released on a milestone basis throughout. Responsive private lenders can often move from application to closing in 30-45 days when the borrower comes prepared, timelines vary by lender and project complexity, so confirm specifics with your lender early.

Choosing the right lender for your project type and scale

Match the lender type to your project scale. Single-lot builds and 1-4 unit investment projects are well-served by private lenders and portfolio lenders that can move quickly and underwrite flexibly around investment-specific criteria. Larger BTR communities and multifamily development projects in the $10M-$50M+ range may require institutional capital with correspondingly large minimum loan sizes. For most individual rental investors building one to four units or a small rental development, a non-bank private lender with direct construction-to-rental expertise is the most efficient path from application to funded project. If your timeline creates a temporary gap between acquisition and permanent financing, you may also consider when a short-term bridge solution fits; learn more about timing and use-cases in our Bridge Loans Explained: What They Are and When to Use One | Cape Henry Capital guide.

Start Building Your Rental Portfolio From the Ground Up

The answer to "can I get a construction loan for a rental property?" is yes, but success depends on choosing the right loan structure, preparing the right documentation, and partnering with a lender who actually understands rental investment underwriting from the construction phase through the long-term hold. Investor construction financing is accessible and well-suited to the projects rental investors are actively pursuing in 2026.

The two most important decisions you'll make are choosing between a one-time-close structure and a construction-only approach, and selecting a lender built to serve investors rather than owner-occupants. Get those two right and the rest of the process is execution.

Cape Henry Capital works specifically with rental investors and builders on ground-up construction financing, from single-lot builds to full BTR developments. Visit capehenrycapital.com to discuss your project and get a no-obligation construction financing quote. Your next rental property can start as a blueprint, Cape Henry Capital is built to fund what comes next.

Tailored loans for real estate investors.

info@capehenrycapital.com

p. 757-267-9495

© Cape Henry Capital, LLC. 2023 All Rights Reserved. NMLS # 2383447.

Capehenrycapital.com is a website operated Cape Henry Capital, LLC, a Delaware limited liability company (“Cape Henry Capital”). By accessing this site and any pages thereof, you agree to be bound by our terms of use and privacy policy. The use of this website does not constitute an application for a mortgage loan or an offer by Cape Henry Capital to lend.

Cape Henry Capital is a mortgage broker and not a lender. Cape Henry Capital is licensed in FL,GA,PA,SC,TX. Please visit www.nmlsconsumeraccess.org for more licensing information.

Mortgage loan products referenced in this website are offered to qualified borrowers for business or commercial purposes only and may be secured by non-owner-occupied properties only.

Origination fees and other fees may apply. Financing is subject to certain restrictions and requirements including, but not limited to, due diligence, credit evaluation, and approval of the subject property. To qualify, borrowers must meet underwriting requirements. Not all borrowers will qualify and not all borrowers that qualify will receive the lowest rate. The actual loan rate and terms depend on a variety of factors. Actual rates, terms, and conditions are subject to change from time to time without notice.

Cape Henry Capital’s principal business address is 500 Studio Drive, Suite 101, Virginia Beach, VA 23452

1340 N. Great Neck Road, Suite 1272, #191 Virginia Beach, VA 23454

Check Out our Newsletter for Market Trends, Updates and Investor Resources