Bridge Loans Explained: What They Are and When to Use One

Want to close deals faster and scale your real estate investing business? Our latest blog breaks down everything investors need to know about bridge loans—from how they work and what they cost to how to qualify and when they make sense for your strategy. Whether you’re flipping properties, buying rentals, or competing for time-sensitive opportunities, this article will help you understand how smart investors use bridge financing to move quickly and maximize profits. Read the full blog to see if a bridge loan is the right tool for your next investment deal

BRIDGE LOANS

Nick Thomas

5/14/20269 min read

You find the deal. The numbers work. But your capital is tied up in another property, or the conventional mortgage timeline will cost you the contract. This is the moment a bridge loan was built for, short-term financing designed for exactly the gap active real estate investors face constantly. A bridge loan covers the financing gap between where you are now and where your deal needs to be, whether that's acquiring a distressed asset before a competitor does, funding a renovation before a DSCR refinance, or stabilizing a value-add property before locking in long-term debt.

At Cape Henry Capital, we offer interest-only bridge loans with terms up to 24 months, specifically structured for real estate investors who need flexible short-term capital without the income verification hurdles of a conventional lender. By the end of this article, you'll know exactly what bridge financing costs, how to qualify, and whether it's the right tool for your next deal or whether an alternative fits better.

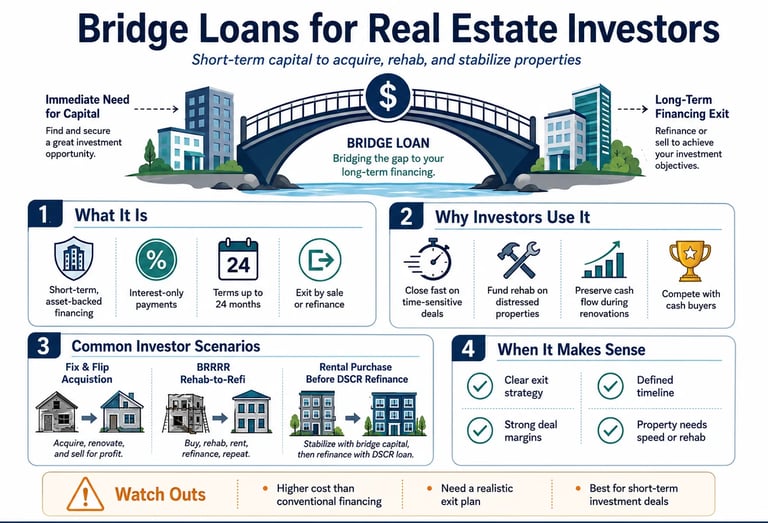

What a Bridge Loan Is and How Investors Actually Use It

A bridge loan is a short-term, asset-backed loan that covers a financing gap between two transactions or phases of a deal. Sometimes called a swing loan or interim mortgage, it uses the property itself as collateral, and repayment happens when the investor sells, refinances into permanent financing, or completes a stabilization event. Unlike conventional mortgages, bridge loans are underwritten primarily on asset value and the exit strategy, not on W-2s or tax returns.

The Gap Bridge Loans Are Designed to Fill

Conventional lenders typically take 30 to 45 days to fund a mortgage. Competitive deals don't wait that long. Bridge financing steps in as temporary mortgage financing, sometimes called a short-term home loan in residential contexts, that keeps deal momentum intact when a traditional approval timeline would kill the opportunity entirely. Sellers in tight markets aren't going to hold a contract for six weeks while a bank processes paperwork.

Three Investor Scenarios Where Bridge Loans Make Sense

Fix-and-flip acquisition: Acquire a distressed property quickly, fund the renovation, then sell or refinance at the improved value.

BRRRR rehab-to-refinance gap: Use a bridge loan to buy and rehab a rental property, then pay it off with a DSCR refinance once the property is stabilized and leased.

Rental acquisition ahead of long-term financing: Close on a rental before a DSCR loan is in place, especially when the property condition doesn't qualify for agency financing yet.

How Bridge Loans Differ from Hard Money Loans

Hard money loans are typically asset-only underwriting with shorter terms, higher rates, and less flexibility on structure. Bridge loans from investor-focused private lenders can include interest-only payment structures, longer terms, and renovation budget coverage. That combination makes them a more versatile tool for investors managing longer rehab timelines or slower lease-up periods.

How Bridge Loans Work: Structure, Terms, and Timelines

Most bridge loans are structured with interest-only monthly payments and a balloon payment at the end of the term. This keeps your monthly carry low during a rehab or stabilization period, preserving cash for renovation costs and operating expenses. A fully amortizing loan would reduce your liquidity exactly when you need it most.

Interest-Only Payments and Why They Matter for Cash Flow

On a $300,000 bridge loan at 10.5% interest-only, your monthly payment is $2,625. A fully amortizing loan at the same rate over 12 months would run significantly higher, eating into the renovation budget month after month. The interest-only structure isn't a concession from the lender. It's a deliberate design that preserves borrower liquidity during short-term rehab and stabilization periods, which is precisely when that liquidity matters most.

LTV Limits and What They Mean for Your Deal Structure

Most bridge lenders cap loan-to-value at 65% to 80%, which means you need meaningful equity in the subject property or a purchase price well below the appraised value. Some lenders will extend higher leverage when the exit strategy is strong and the borrower has a documented track record. Understanding the LTV ceiling upfront lets you structure the deal correctly before you're at the closing table.

From Application to Funded: The Typical Timeline

Bridge loans can approve in roughly 72 hours and fund within one to two weeks for clean deals. Compare that to the 30 to 45 days typical of a conventional mortgage, and the speed advantage is clear. For lenders' overviews of how bridge loans work in practice, see our bridge loan requirements. For investors competing against cash buyers or dealing with sellers who have short acceptance windows, this timeline difference is often what separates a closed deal from a lost one.

What Bridge Financing Actually Costs

Bridge loan interest rates currently run between 8.5% and 12%+ for most residential investment products. That's higher than conventional mortgage rates, and it's supposed to be. You're paying for speed, flexibility, and underwriting based on the property rather than your personal income history. The rate premium is the cost of not waiting 45 days. For a concise industry overview of bridge loan rates, fees, and closing costs, contact Cape Henry Capital for a free consultation.

Interest Rates: What to Expect and Why They're Higher Than Conventional

Conventional mortgages run 6% to 7% for investment properties. Bridge loans run 8.5% to 12%+. The difference reflects shorter terms, faster underwriting, and the lender's exposure during a rehab or transition period. This isn't a penalty. It's the market price for short-term, flexible capital that doesn't require two months of income documentation.

Fees That Add Up Fast If You're Not Watching

Beyond the interest rate, expect origination fees of 0.5% to 2% of the loan amount. Closing costs typically range from roughly 1% to 3% depending on state, title fees, and lender, many transactions fall in the 1% to 2% range, though complex deals can run higher. Budget for an appraisal in the $300 to $600 range and potential prepayment penalties of 1% to 2% if you pay off early. Bridge loans in 2026 have evolved and many bridge loan options do not have a prepayment penalty. Many investors focus on the rate and miss the total all-in cost. Underwrite the full picture, not just the headline number.

Running the Real Numbers Before You Commit

On a $250,000 bridge loan at 10.5% interest-only for nine months, your interest carry is roughly $19,688. Add a 1.5% origination fee ($3,750) and $4,000 in closing costs, and your total financing cost for the nine months runs approximately $27,438. If your deal produces a $60,000 profit after renovation, that cost structure works. If the margins are thin, the math tells you before you commit.

How to Qualify for a Bridge Loan

Credit score minimums typically start at 600 to 680 with most private bridge lenders, though some flexibility exists when the asset and exit plan are strong. Debt-to-income ratio is not a factor for a commercial bridge loans; however, most lenders will want to see at least six months of liquidity reserves in a bank account to ensure a borrower is able to make their monthly payments. These are baseline thresholds, not automatic approvals.

Credit, Equity, and LTV: The Baseline Requirements

Private lenders evaluate borrower profiles differently than banks. A self-employed investor with a complex tax return isn't disqualified just because their W-2 is zero. When the asset value is strong, the equity position is solid, and the exit plan is clearly defined, lenders have room to work with non-traditional borrower profiles that conventional underwriting would reject outright. Bridge loan requirements are focused more on the proprety, the exit strategy, and the experience of the borrower.

Why Your Exit Strategy Is the Real Underwriting Factor

The single most important element in a bridge loan application is the exit strategy. Lenders want to see exactly how the loan gets repaid: a signed sale contract, a pending DSCR refinance, or a documented lease-up timeline. A vague plan is the top reason bridge loans get denied or end in default. Be specific, be realistic, and put it in writing before you apply.

What Documentation Bridge Lenders Typically Require

Bridge loan documentation packages are shorter than conventional mortgage files. Expect to provide a credit pull, property details and appraisal, two to three months of bank statements, and a written exit strategy. The process is designed to move quickly, which means the underwriter needs clean, organized information rather than a full financial history. Come prepared and the timeline holds.

Bridge Loans vs. HELOCs and Other Short-Term Alternatives

Not every financing gap requires a bridge loan. HELOCs, contingent offers, and bridge-to-permanent products all serve different scenarios. Understanding where each tool fits helps you choose the right one instead of defaulting to the most familiar option.

Bridge Loans vs. HELOCs: Speed and Flexibility vs. Lower Cost

HELOCs average around 7.4% in interest, which is lower than a bridge loan. But they take four to six weeks to fund, require existing equity in a separate property, and are often not feasible as direct acquisition financing for a new purchase, many lenders restrict this use outright. For an investor trying to close a deal in two weeks, a HELOC isn't realistic regardless of the rate. Speed and flexibility are worth the rate premium when a deal has a firm close date.

Contingent Offers and Why Sellers Often Reject Them

A contingent offer ties your purchase to the sale of another property, which signals to sellers that your financing is uncertain. In competitive markets, sellers frequently reject contingent offers in favor of buyers who can close without conditions. Even when sellers accept them, the added complexity slows the timeline and compounds holding costs if the contingency takes longer than expected to clear.

Bridge-to-Permanent Loans: When They Make Sense

A bridge-to-permanent loan converts short-term financing into long-term debt after a stabilization or construction phase completes. This structure is most common in commercial real estate and new construction projects, where the path from ground-breaking to stabilized occupancy is well-defined. For standard fix-and-flip or BRRRR scenarios, a standalone bridge loan followed by a separate DSCR refinance is typically more flexible and easier to execute.

When a Bridge Loan Fits Your Investment Strategy (and When to Walk Away)

Bridge financing works best when the timeline is defined, the exit strategy is proven, and the deal math supports the higher cost of capital. If any of those conditions are missing, the loan can turn a good deal into a difficult situation fast. Carry two debt obligations while a sale stalls, and the monthly pressure compounds quickly.

Investor Scenarios Where Bridge Financing Clearly Wins

Bridge loans are the right call when you're acquiring a distressed asset before a competing offer lands, funding a rehab that conventional lenders won't touch due to property condition, or bridging the gap in a BRRRR strategy before a DSCR refinance is ready. In each case, the deal has a clear end state, a realistic timeline, and a financing structure that supports the margin.

Red Flags That Signal a Bridge Loan Is the Wrong Move

Walk away from bridge financing when you don't have a confirmed exit strategy, when the deal only works at an optimistic ARV that hasn't been validated, or when local market data shows inventory building and sale timelines stretching. For context on how long properties typically take to sell and how that can affect your exit plan, see Zillow's average time to sell a house. That kind of market shift can turn a 6-month bridge into a default if the exit was built on a quick-sale assumption.

Finding a Bridge Lender Built for Investors

Cape Henry Capital offers interest-only bridge loans with terms up to 24 months, structured for investors who need more runway than shorter-term products typically allow. Funding timelines are designed to move fast, you work directly with underwriters, and income verification requirements are minimal compared to conventional lenders. If your deal has a clear exit and the numbers work, contact Cape Henry Capital to discuss your scenario and get a customized loan quote.

Know Your Costs, Know Your Exit, and Move Faster Than the Competition

A bridge loan is a powerful tool when the deal math is solid and the exit is defined. The costs are real: 9.5% to 12% in interest, 0.5% to 2% in origination, and closing costs that typically land between 1% and 3% depending on your market and lender. Underwrite all of it, not just the rate. When the profit margin absorbs those costs and the exit is credible, bridge financing lets you close deals that slower capital simply cannot touch.

Qualification comes down to the asset, the equity position, and the exit strategy. Investors who can clearly articulate how the loan gets repaid, whether through a sale, a DSCR refinance, or a documented stabilization event, are the ones who get approved and funded quickly. That clarity is what separates investors who use bridge loans effectively from those who end up in default.

Investors who understand how to deploy short-term financing as a strategic lever close deals that conventional timelines can't reach, and compound that advantage across every cycle. If you're ready to see whether a bridge loan fits your next deal, explore Cape Henry Capital's bridge loan terms or run your scenario through the bridge loan calculator to know your numbers before you bid.

Tailored loans for real estate investors.

info@capehenrycapital.com

p. 757-267-9495

© Cape Henry Capital, LLC. 2023 All Rights Reserved. NMLS # 2383447.

Capehenrycapital.com is a website operated Cape Henry Capital, LLC, a Delaware limited liability company (“Cape Henry Capital”). By accessing this site and any pages thereof, you agree to be bound by our terms of use and privacy policy. The use of this website does not constitute an application for a mortgage loan or an offer by Cape Henry Capital to lend.

Cape Henry Capital is a mortgage broker and not a lender. Cape Henry Capital is licensed in FL,GA,PA,SC,TX. Please visit www.nmlsconsumeraccess.org for more licensing information.

Mortgage loan products referenced in this website are offered to qualified borrowers for business or commercial purposes only and may be secured by non-owner-occupied properties only.

Origination fees and other fees may apply. Financing is subject to certain restrictions and requirements including, but not limited to, due diligence, credit evaluation, and approval of the subject property. To qualify, borrowers must meet underwriting requirements. Not all borrowers will qualify and not all borrowers that qualify will receive the lowest rate. The actual loan rate and terms depend on a variety of factors. Actual rates, terms, and conditions are subject to change from time to time without notice.

Cape Henry Capital’s principal business address is 500 Studio Drive, Suite 101, Virginia Beach, VA 23452

1340 N. Great Neck Road, Suite 1272, #191 Virginia Beach, VA 23454

Check Out our Newsletter for Market Trends, Updates and Investor Resources