DSCR Loans Explained: Qualify on Rental Cash Flow Fast

DSCR loans give real estate investors a smarter way to qualify for rental property financing by focusing on the property’s income instead of personal income documentation. This guide explains how debt service coverage ratio loans work, how to calculate DSCR, what lenders typically require for credit, down payment, and reserves, and why this financing option can be a strong fit for self-employed investors, portfolio builders, and borrowers who do not fit the conventional lending box.

DSCR LOANS

Nick Thomas

6/5/20269 min read

Most rental property investors get rejected by conventional lenders not because the deal is bad, but because their personal income doesn't look right on paper. A W-2 from a day job or a complex self-employed tax return shouldn't be the reason a cash-flowing property doesn't get funded. The property is the asset. It either pays for itself or it doesn't. If your rental cash flow is strong but your tax return works against you, a DSCR loan qualifies the deal on what actually matters, the property's income, not yours.

A debt service coverage ratio loan solves exactly this problem by qualifying you based on what the property earns. Specialized private lenders like Cape Henry Capital have built their entire model around this approach, helping serious investors scale rental portfolios without hitting the income verification wall that stops deals at conventional banks.

This article breaks down what a DSCR loan is, how to calculate your ratio, what lenders actually require, and how to apply without the documentation burden of a conventional mortgage.

Explore Cape Henry Capital’s DSCR loan program for real estate investors.

What a DSCR Loan Is and How It Differs from Conventional Financing

The core principle: the property qualifies, not you personally

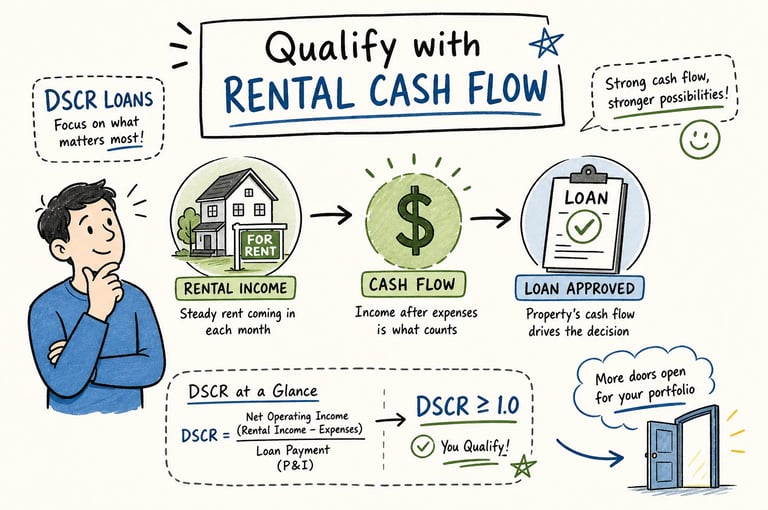

A DSCR loan is a real estate investment loan underwritten on the property's cash flow. The central metric is the Debt Service Coverage Ratio: net operating income divided by annual debt service. Lenders are asking one question: does this property generate enough income to cover its own mortgage payments?

Conventional underwriting asks a completely different question: can the borrower personally afford this loan? That means W-2s, two years of tax returns, employment verification, and a full debt-to-income calculation based on your personal income. If you have write-offs, multiple entities, or inconsistent income year-to-year, that model works against you even when your properties are cash-flowing well.

Why this matters for self-employed and portfolio investors

Many real estate investors look poor on paper despite owning profitable rentals. Business owners who maximize deductions, investors with income spread across multiple LLCs, and anyone without a predictable W-2 salary all run into this problem with conventional lenders. The tax return shows low taxable income by design, and banks penalize you for it.

This non-QM DSCR loan structure removes the income verification barrier entirely for qualifying purposes. The product was specifically built for rental portfolio investors, BRRRR strategy investors, self-employed buyers of investment properties, and anyone whose real-world financial strength doesn't translate cleanly to a 1040. If the property cash flows, the conversation starts.

How to Calculate DSCR for a Rental Property

The DSCR formula and what each variable means

The formula is simple: DSCR = Net Operating Income (NOI) ÷ Annual Debt Service.

NOI is calculated by taking gross rental income and subtracting operating expenses. These expenses typically include property taxes, insurance, HOA dues, property management fees, maintenance, and other routine costs of operating the property. The mortgage payment itself is not included in NOI because it is accounted for separately as debt service.

Annual debt service is the property’s total yearly mortgage obligation, including principal and interest. If you only know the monthly payment amount, multiply it by 12 to calculate the annual debt service.

A DSCR above 1.0 means the property generates enough income to cover its debt payments. A DSCR below 1.0 means the property does not generate enough income to fully cover its debt.

Two worked examples using real numbers

Example 1: A single-family rental earns $60,000 in gross annual rent. Operating expenses total $22,000, leaving an NOI of $38,000. The annual debt service on the proposed loan is $30,000. DSCR equals $38,000 divided by $30,000, which comes out to 1.27. That means the property generates 27% more income than it needs to cover the mortgage. Most lenders will approve this deal and the borrower gets competitive pricing.

Example 2: A larger rental earns $80,000 gross annually, but after applying a 5% vacancy allowance ($4,000), the effective income drops to $76,000. Subtract $26,000 in operating expenses and the NOI is $50,000. The proposed mortgage carries a $3,500 monthly payment, or $42,000 annually. DSCR equals $50,000 divided by $42,000, landing at 1.19. That clears the 1.00 minimum most lenders require, though it sits below the 1.25 threshold that typically unlocks the best rates and terms.

Using a DSCR calculator before you apply

Running these numbers before talking to a lender saves time and shows clearly whether a deal pencils out at your expected purchase price and financing terms. It also lets you test scenarios: what happens if you put 25% down instead of 20%, or if market rents come in slightly lower than projected? Cape Henry Capital offers a free DSCR loan calculator that walks through exactly these scenarios for investor cash flow loan underwriting, so you can stress-test a deal before committing to an offer. For additional perspective on calculating DSCR and practical examples, review guidance on how to calculate DSCR loans efficiently.

What Lenders Look For: DSCR Thresholds, Credit, and Down Payment

Minimum DSCR ratios and how they affect your rate

Most lenders require a minimum DSCR between 1.00 and 1.25. A ratio of 1.25 or above typically unlocks the best pricing and the highest available leverage. Some lenders will approve deals below 1.00, but those approvals come with conditions: more equity, stronger credit scores, and higher liquid reserves required at closing.

The tradeoff is direct. A stronger ratio gives the lender more confidence in the property's ability to sustain payments through vacancy or expense spikes, and that confidence translates into better loan terms. Don't treat the minimum as a target. Deals that barely clear the floor tend to carry rate adjustments that eat into your returns. For an institutional view of how DSCR factors into commercial lending, see this primer on what is debt service coverage ratio (DSCR) in real estate.

Credit score, down payment, and reserve requirements

Minimum credit scores for most DSCR programs fall in the 620 to 660 range. Better pricing typically starts at 700 and above, with some lenders offering notable rate improvements at 740 or higher. The credit score requirement is looser than conventional financing, but it still matters for where your rate lands.

Standard down payment requirements sit at 20 to 25%, corresponding to 75 to 80% LTV on purchase transactions. Lenders also require reserves, usually six months of the fully loaded housing payment (principal, interest, taxes, insurance, and any HOA fees) held in liquid accounts, though some programs accept three months for stronger files. The stronger your DSCR, credit score, and reserve position, the better your terms will be across the board. Each variable affects the others, so improving one can partially offset weakness in another.

What Documents DSCR Lenders Actually Need (and What They Skip)

What you don't have to provide

No personal tax returns for income verification. No W-2s. No pay stubs. No employer letters. No personal debt-to-income calculation derived from your salary or business income. For self-employed investors and those with complex financials, this is the part that changes everything. The file doesn't require you to justify how you earn a living.

This is how debt service coverage ratio financing is structured by design. The underwriting decision is based on the asset's cash flow performance. Your personal income profile isn't the relevant variable, and removing it from the equation means the file moves faster and fits more investors who own profitable properties but look complicated on a 1040.

What goes into a standard DSCR loan file

The documentation stack is focused on the property and your liquid assets. Here's what a typical file includes:

Lease documentation: a signed lease agreement showing rent, term, and tenant details. For vacant properties, a market rent analysis or appraisal rent schedule (Form 1007 for single-family, Form 1025 for multi-unit) substitutes for an active lease.

Bank and asset statements: two to three months of recent statements to verify reserves, down payment source, and liquid assets.

Property documents: purchase contract, current mortgage statement for refinances, property tax bill, insurance binder, and HOA statement if applicable.

Standard closing items: appraisal, title, government-issued ID, and if the loan is held in an entity, LLC operating agreement and EIN letter.

The process is cleaner and faster than a conventional mortgage file because the underwriting question is narrower. The property needs to qualify on cash flow, and the documentation exists to confirm that picture.

DSCR Loans vs. Conventional Mortgages: Rates, Terms, and Tradeoffs

Where the cost difference actually comes from

DSCR financing typically prices one to two percentage points above conventional investment-property loans because the lender underwrites without verifying personal income, which carries additional risk in their model. Based on current lender pricing as of mid-2026, competitive rates for strong single-family rental files are generally in the 6.25% to 7.5% range, while conventional investment property rates tend to run around 7.1% to 7.6% for qualified W-2 borrowers. The gap has narrowed compared to prior years, but it still exists.

Beyond the rate, factor in origination costs. These loans often come with one to five points upfront, and many include prepayment penalties structured as step-down penalties over one to five years. Loan terms include 30-year fixed, 40-year fixed, interest-only, and ARM options depending on the lender. The interest-only option can be a useful tool for investors optimizing monthly cash flow during a value-add period.

When a DSCR loan makes more sense than going conventional

This type of debt service coverage financing wins in specific situations: self-employed borrowers with significant write-offs, investors who've already hit the conventional loan property limit (typically 10 financed properties), and those building a portfolio faster than their income documentation can support. If your tax return shows $40,000 in net income but you own properties generating $200,000 in gross rents, a conventional lender sees the $40,000. A DSCR lender sees the properties.

Conventional financing may be the better choice for primary residence buyers, borrowers with clean W-2 income and only a few investment properties, or situations where the rate differential meaningfully compresses the deal's returns. The decision isn't one-size-fits-all. It's a strategic call based on your income profile, your portfolio size, and how fast you're moving. For a practical comparison, see this industry guide on DSCR loans vs. conventional loans.

How to Get Started with Cape Henry Capital

What makes a private DSCR lender different from a bank

Banks move slowly, layer on documentation requirements, and often cap how many investment properties they'll lend on in the first place. Their underwriting systems weren't built for investors with portfolios, entities, or income that doesn't fit a standard pay stub. By the time you submit everything they ask for, conditions keep coming and deals fall apart.

Private lenders like Cape Henry Capital qualify on cash flow from the first conversation, move faster through underwriting, and work specifically with investors who have non-traditional income profiles. There are no middlemen between you and the person making the credit decision. Underwriters who understand investment real estate are directly accessible, and that makes the process faster and less frustrating for borrowers who know their deals.

Cape Henry Capital's DSCR process from application to quote

The process starts with a prequal that takes under 10 minutes. Submit basic property and borrower information, and you get an instant prequal letter the same day. No obligation, no lengthy intake call required. From there, a full loan evaluation and rate quote comes within 24 hours so you know exactly where you stand before moving forward.

Cape Henry Capital offers 30-day rate locks with instant rate quotes after underwriting review, which gives you certainty while you navigate a purchase timeline. The process is built for investors whose income profiles don't fit the conventional mold, self-employed borrowers, active portfolio builders, and anyone who's scaled past what traditional bank lending allows. When speed and clarity matter, the workflow is designed to deliver both.

The Bottom Line on Debt Service Coverage Ratio Financing

A DSCR loan removes the income verification barrier by letting the property speak for itself. The ratio tells the lender whether the asset generates enough cash flow to carry its own debt, and if it does, your W-2 status becomes irrelevant to the approval. That's a fundamentally different model from conventional mortgage underwriting, and for real estate investors, it's a better fit.

To recap the key points: the ratio is NOI divided by annual debt service, with 1.25 or above putting you in the strongest position. You'll need 20 to 25% down, a credit score of 660 or better for competitive pricing, and six months of reserves. You won't need tax returns or pay stubs. The file is about the property, the lease, and your liquidity.

If your rental property cash flows but your personal income doesn't qualify you for a conventional mortgage, this is the right financing structure. Start by running your numbers in Cape Henry Capital's free DSCR Calculator to see exactly where your ratio lands. Then get an instant prequal letter so you know your position before you make an offer. For quick answers to common issues, check our DSCR Loan FAQs for Real Estate Investors. The deal either works or it doesn't, and you can find out in a few minutes.

Tailored loans for real estate investors.

info@capehenrycapital.com

p. 757-267-9495

© Cape Henry Capital, LLC. 2023 All Rights Reserved. NMLS # 2383447.

Capehenrycapital.com is a website operated Cape Henry Capital, LLC, a Delaware limited liability company (“Cape Henry Capital”). By accessing this site and any pages thereof, you agree to be bound by our terms of use and privacy policy. The use of this website does not constitute an application for a mortgage loan or an offer by Cape Henry Capital to lend.

Cape Henry Capital is a mortgage broker and not a lender. Cape Henry Capital is licensed in FL,GA,PA,SC,TX. Please visit www.nmlsconsumeraccess.org for more licensing information.

Mortgage loan products referenced in this website are offered to qualified borrowers for business or commercial purposes only and may be secured by non-owner-occupied properties only.

Origination fees and other fees may apply. Financing is subject to certain restrictions and requirements including, but not limited to, due diligence, credit evaluation, and approval of the subject property. To qualify, borrowers must meet underwriting requirements. Not all borrowers will qualify and not all borrowers that qualify will receive the lowest rate. The actual loan rate and terms depend on a variety of factors. Actual rates, terms, and conditions are subject to change from time to time without notice.

Cape Henry Capital’s principal business address is 500 Studio Drive, Suite 101, Virginia Beach, VA 23452

1340 N. Great Neck Road, Suite 1272, #191 Virginia Beach, VA 23454

Check Out our Newsletter for Market Trends, Updates and Investor Resources