BRRRR Financing: The Two-Phase Loan Playbook for Investors

Learn the two-phase BRRRR financing playbook: which bridge and DSCR loans to use, LTVs, rates, seasoning rules, and how to plan your refinance.

BRRRRDSCR LOANSFIX & FLIP LOANSBRIDGE LOANS

Nick Thomas

6/30/202611 min read

If you're wondering what loans work best for the BRRRR method, the answer isn't a single product, it's a sequenced two-phase strategy. Most investors searching for BRRRR financing ask the wrong question. They want to know which one loan carries a deal from distressed acquisition through long-term rental hold. No loan does that. The BRRRR strategy is a two-phase structure by design, and treating it as a one-loan problem is the fastest way to kill your deal's profitability before the renovation even starts.

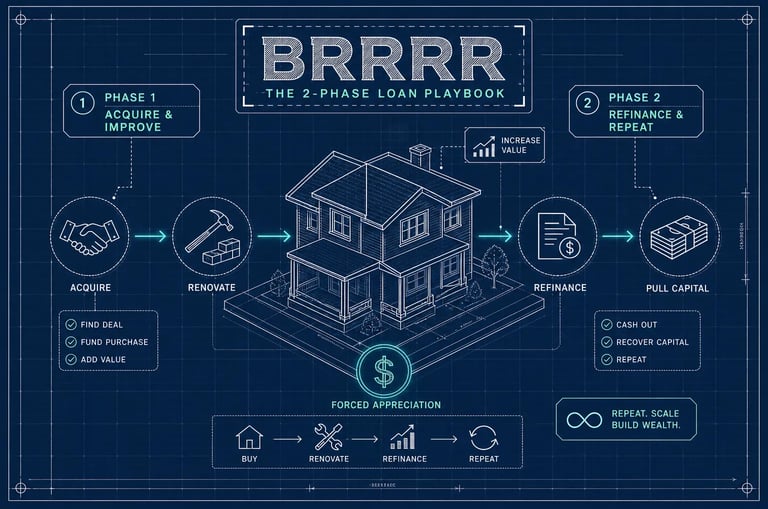

Phase 1 is the entry: a short-term bridge or rehab loan that funds the acquisition and renovation. Phase 2 is the exit and reset: a DSCR refinance that converts short-term debt into permanent financing and returns your capital for the next deal. Both phases have distinct loan structures, underwriting criteria, and cost profiles. Understanding how they connect is what separates investors who scale from investors who stall.

This guide breaks down both phases with real numbers: LTV ratios, rate ranges, seasoning windows, and DSCR thresholds. It also covers where most investors lose time between phases and how to plan the refinance exit before you ever sign a purchase contract. Cape Henry Capital offers both products in-house for investors who want to run the full cycle without switching lenders mid-deal.

What Loans Work Best for the BRRRR Method, And Why It Takes Two

The BRRRR cycle has two fundamentally different financial problems. The first is acquiring and renovating a distressed property quickly, often in a competitive market, with a financing structure that covers both the purchase price and the rehab budget. The second is holding a stabilized rental property long-term at a payment level that cash-flows. No single loan product solves both problems well.

A 30-year DSCR loan won't fund a distressed acquisition. These loans require the property to already be in rentable condition and generating income. Trying to force a long-term rental loan onto a value-add deal leaves the renovation budget unfunded and the acquisition timeline uncompetitive. On the other side, a 12-month bridge loan at 11, 12% annual interest isn't something you want holding a stabilized rental. The carrying cost destroys cash flow and eats into the equity you're preserving for the refinance.

It's also worth knowing what doesn't fit the BRRRR loan strategy at all. FHA 203(k) loans, for instance, allow renovation financing but require owner-occupancy, impose strict contractor approval processes, and close far too slowly for competitive distressed acquisitions. Private or portfolio loans from community banks can bridge some gaps, but they rarely offer the combined LTC flexibility and speed that purpose-built bridge products deliver. The BRRRR loan strategy works best when each phase uses the product actually designed for it.

How the Two Phases Divide the BRRRR Cycle

Phase 1 covers the Buy and Rehab steps. This is an asset-based, short-term loan with a draw-funded renovation component. The lender underwrites the property's value and your exit plan, not your personal income. Phase 2 covers the Rent, Refinance, and Repeat steps. Once the property is stabilized with a tenant in place, you refinance into a long-term DSCR loan that qualifies on the property's rental income and pulls your capital back out.

The transition between phases is where most BRRRR deals lose momentum. The renovation finishes, the tenant moves in, and the investor scrambles to find a DSCR lender, restart an underwriting process, and close before the bridge loan term expires. Every week of delay in that gap adds carrying costs on a loan already running at 10, 14% annually. Planning both phases before funding Phase 1 is not optional. It is the core skill the strategy demands.

Why Most Investors Run Into Trouble Between Phases

The gap risk is real and underappreciated. Consider a typical deal: an investor acquires a property for $150,000 with a $40,000 rehab budget, a $190,000 commitment, without a confirmed Phase 2 exit. If the bridge loan matures before the DSCR refi closes, extension fees pile up fast. Lenders commonly charge an additional percentage of the loan balance per extension period on top of the ongoing interest rate, and those costs can erode months of equity gains quickly.

The fix is to plan backward. Before you fund the acquisition, know your target refinance value, confirm you can hit the DSCR threshold at that value with current market rents, and verify you have a lender who can execute the Phase 2 loan within your bridge term. Lock in that exit logic first, then fund the entry.

Phase 1: Best Loans for BRRRR Acquisitions and Renovation

Bridge loans, also called hard money or rehab loans, are the standard tool for BRRRR acquisitions. They're short-term, asset-based loans structured to fund a distressed purchase and renovation budget in a single closing. The underwriting process doesn't require W-2s, tax returns, or income verification. Approval is driven by the property's current value, its projected after-repair value (ARV), and the investor's exit strategy.

This is why hard money loans dominate competitive acquisitions. Specialized bridge lenders close in three to five business days, letting investors compete alongside cash buyers on distressed listings. A conventional mortgage requiring 30, 45 days to close simply isn't a viable tool at this stage of the cycle.

LTV, LTC, and How Lenders Size the Phase 1 Loan

Two metrics control how much a bridge lender will fund. LTV (loan-to-value) is calculated against the purchase price and typically runs 65, 80%. LTC (loan-to-cost) covers the total project cost, purchase price plus rehab budget, and can reach 80, 95% depending on the lender and the borrower's experience level. The ARV (after-repair value) functions as the ceiling: most lenders cap total financing at 70% of the projected post-renovation appraised value.

A concrete example: a $150,000 purchase with a $40,000 rehab budget creates a total project cost of $190,000. At 85% LTC, the lender funds $161,500. If the ARV is $250,000, the 70% ARV cap allows up to $175,000, so the LTC calculation is the binding constraint in this scenario. Run both numbers on every deal and understand which constraint limits the loan before committing to a purchase price.

Interest Rates, Points, and Term Lengths to Expect

In 2026, bridge loans for BRRRR projects are pricing between 8.75% and 14.5% annually for most transitional deals. Higher-leverage or higher-risk projects sit closer to the top of that range; experienced borrowers with lower LTV deals can access rates nearer to 8.75, 9%. Origination points run 2, 3% of the loan amount upfront at closing, with some lenders charging up to 5% on high-leverage options.

Term lengths are typically 12, 18 months, with 12 months being the most common structure for standard BRRRR timelines. Most loans are interest-only during the term, which keeps monthly carrying costs manageable while the renovation is underway. Extensions are available at most lenders but carry additional fees, which is exactly the gap-risk scenario you avoid by planning the Phase 2 exit before you close Phase 1.

For current market context on expected borrowing costs, see recent analysis of bridge loan rates in 2026.

How Rehab Draw Schedules Actually Work

The renovation budget is not released at closing. Lenders hold those funds in escrow and release them in stages as work is completed and verified by inspection. You pay contractors first, then submit a draw request with photos, invoices, and lien waivers. The lender sends an inspector, typically within one to two business days, and releases funds once the milestone is confirmed. Reimbursement usually hits within one to three business days after inspection.

A realistic draw structure for a $75,000 rehab might look like this: an initial draw at closing for materials, a second draw at 30, 40% completion covering rough-ins and structural work, a third draw at 70, 75% completion for drywall and mechanical installations, and a final draw at certificate of occupancy. The key operational requirement is working capital: you need cash available to float each phase before the reimbursement arrives. Investors who underestimate this float requirement stall their own rehab timelines.

What Lenders Evaluate Before Funding Phase 1

Bridge loan approval is not automatic. Lenders are underwriting a deal, not a person, but the deal still needs to meet clear criteria. The difference between a three-day close and a three-week close usually comes down to how clean the property analysis and investor documentation are at submission.

Property Criteria and ARV Requirements

The ARV is the central number because it's the collateral basis for the loan. Lenders validate ARV through comparable sales: properties within roughly one mile, similar square footage, and in comparable condition post-renovation. Weak comparable data or properties in declining markets face tighter LTV caps. Extreme structural issues, such as foundation problems or major environmental concerns, can disqualify a deal or significantly reduce the loan amount.

The ARV analysis also needs to support a clean Phase 2 exit. If the appraiser's comp data won't hold up at refinance time, the DSCR refi appraisal will come in low and your capital recovery shrinks. Lenders who specialize in BRRRR financing think about this alignment proactively. It's worth asking any bridge lender how they evaluate the refinance path at origination.

Borrower Experience and Credit Thresholds

Bridge lenders don't ask for income documentation, but they do review credit and track record. Minimum credit scores for most programs run 620, 660, with better pricing available above 700. Experienced investors, typically defined as two or more prior completed flips or rental acquisitions, often access higher LTC ratios and lower rate tiers. First-time investors can still qualify on most programs but should expect tighter LTV limits and a larger equity requirement at acquisition.

Phase 2: The DSCR Refinance That Restocks Your Capital

Once the renovation is finished and a tenant is in place, Phase 2 begins. The DSCR refinance converts short-term bridge debt into permanent financing and returns the investor's capital for the next cycle. This is the mechanism that makes "Repeat" in BRRRR actually executable at scale rather than just aspirational.

Seasoning Requirements and When You Can Refinance

Most DSCR lenders require a minimum six-month seasoning period: the investor must have held the property for at least six months from the original purchase closing date before a cash-out refinance is permitted. Some lenders impose a 12-month requirement, so confirming this upfront with your Phase 2 lender is critical. The bridge loan term needs to cover this seasoning window entirely, meaning an investor closing the rehab in month three still carries two to three months of bridge loan cost before the DSCR refi can close.

A limited exception exists for all-cash purchases using delayed financing, where no seasoning requirement applies. For standard bridge-financed BRRRR deals, six months is the floor. If your rehab timeline is aggressive, consider selecting an 18-month bridge term rather than a 12-month term to give the seasoning period room to clear without forcing an extension.

Max LTV and How Much Equity You Can Actually Pull

DSCR cash-out refinances typically cap at 70, 75% LTV on the post-rehab appraised value. Running the numbers on a concrete example: a property appraising at $250,000 post-renovation with a 75% LTV cap supports a loan of $187,500. If the total cost basis, purchase price plus rehab budget plus closing costs, was $160,000, the investor recovers approximately $27,500 in net capital after the refinance pays off the bridge loan.

The quality of the rehab determines the refinance appraisal, which directly determines the capital recovery. Cutting corners on finishes can reduce ARV significantly, the savings on renovation often come at a steep cost in appraised value. Quantify that trade-off with market comps before you make finish-level decisions. The Phase 1 and Phase 2 economics are tightly linked; what you spend on the renovation is an input into the refinance output.

How Lenders Calculate DSCR and the Minimum Threshold

The DSCR formula works like this: gross monthly rental income divided by total monthly debt service, principal, interest, taxes, insurance, and any HOA fees. A ratio of 1.0 means rent exactly covers the payment. A ratio of 1.25 means rent covers 125% of the obligation. Most DSCR lenders require a minimum ratio of 1.0 to 1.25 to qualify for standard programs.

One important detail: lenders typically use the market rent figure from the appraisal, not the actual lease amount, when calculating DSCR at refinance. If the current tenant is below market rent, the appraisal's market rent figure may still support the required ratio even when the actual lease falls short. This can mean the difference between qualifying and not qualifying on a deal where rents weren't pushed to market at lease-up.

For a concise overview of common DSCR loan requirements and how lenders approach debt-service coverage, consult the lender-focused resources that summarize underwriting rules for property-income qualification.

DSCR Loans vs. Conventional Mortgages for the BRRRR Refinance

Many investors reach for conventional financing at the refinance stage because the interest rate is lower. On BRRRR deals specifically, that calculation often misses several constraints that make conventional mortgages impractical or impossible as the portfolio grows.

Where Conventional Mortgages Fall Short for Repeat Investors

Conventional investment mortgages cap at 10 financed properties total across all lenders. They also require W-2 income or full tax return verification, and the underwriting process factors in depreciation deductions that reduce an investor's paper income significantly. A self-employed investor or someone with five rental properties already on Schedule E can find themselves unable to qualify for a conventional investment mortgage even when every property they own cash-flows strongly.

What DSCR Loans Do Differently

DSCR loans underwrite the property, not the person. No W-2s, no tax returns, no DTI calculation. The only income variable is the property's rent-to-debt ratio, which means qualifying doesn't get harder as the portfolio grows. An investor with 12 rental properties can add a 13th using a DSCR loan with the same underwriting process as the first one.

The trade-off is a higher interest rate, typically 1, 2% above conventional rates, and prepayment penalties that usually run two to five years. For investors planning to hold properties long-term, neither trade-off is a deal-breaker. For investors planning to sell within the prepayment penalty window, the cost structure changes meaningfully. Know your hold timeline before committing to a DSCR refinance at Phase 2.

How to Find a Lender Built for the Full BRRRR Cycle

Searching for a bridge lender at acquisition and then hunting for a DSCR lender six months later introduces friction at exactly the moment when speed and continuity matter most. The best loans for BRRRR work as a coordinated system, and the right lender makes that coordination possible from day one.

The Real Cost of Switching Lenders Between Phases

Switching lenders mid-cycle means two separate underwriting processes, two sets of closing costs, and two appraisers who may produce conflicting valuations on the same property. It also means the DSCR lender starts from scratch on a deal the investor has been working for six months, with no familiarity with the original purchase price, the rehab scope, or the ARV analysis that supported the bridge loan. Every redundant underwriting step burns time and money.

Across multiple BRRRR cycles per year, this operational drag becomes a real constraint on how fast an investor can scale. Closing three BRRRR deals annually with separate Phase 1 and Phase 2 lenders means six separate underwriting processes, six separate appraisals, and six separate closing cost events. That's a significant amount of friction to build into a repeatable strategy.

What to Look for in a BRRRR-Capable Lender

The right lender offers both bridge and DSCR products in-house, has direct underwriting access without broker intermediaries, closes bridge loans in under 10 business days, and can give you a DSCR rate quote on the stabilized property at the time of bridge loan origination. That last point is critical. If a lender can't tell you what the Phase 2 refinance looks like before you fund Phase 1, you're committing capital without a validated exit.

Both bridge and DSCR products available under one roof

Direct underwriter access with no broker middlemen

Ability to pre-qualify the DSCR exit at bridge loan origination

Bridge loan closes in under 10 business days

No personal income verification on either product

How Cape Henry Capital Structures the Full BRRRR Cycle

Cape Henry Capital offers both bridge loans explained and DSCR refinances as in-house products, which means investors run the full BRRRR cycle without switching lenders between phases. The bridge loan covers acquisition and renovation with interest-only payments during the loan term, and the DSCR refinance on the back end qualifies strictly on property cash flow with no personal income verification required. Both products are handled by the same lending team, which preserves deal context and reduces the redundant underwriting that slows investors down when they switch lenders mid-cycle.

For investors running multiple BRRRR deals simultaneously, that continuity compounds into a real operational advantage over the course of a year. Reach out to Cape Henry Capital to discuss your deal and confirm how the two-phase structure fits your timeline and target markets.

The BRRRR Playbook in Two Clear Phases

Ultimately, what loans work best for the BRRRR method comes down to a sequenced answer: a bridge or rehab loan to acquire and renovate, followed by a DSCR cash-out refinance to stabilize, recover capital, and repeat. The numbers at each phase, LTV ratios, DSCR thresholds, seasoning windows, and rate spreads, connect directly to each other. Investors who plan both phases before funding the acquisition close faster, recover more capital, and scale further than those who treat each phase as a separate problem.

Cape Henry Capital offers a free deal analysis and pre-qualification to help investors stress-test both phases of the financing structure before committing to a purchase. Contact Cape Henry Capital to run your numbers, get a pre-qualification letter, and go into your next acquisition knowing exactly how the full cycle finances. Start with Cape Henry Capital before you make your next offer.

Tailored loans for real estate investors.

info@capehenrycapital.com

p. 757-267-9495

© Cape Henry Capital, LLC. 2023 All Rights Reserved. NMLS # 2383447.

Capehenrycapital.com is a website operated Cape Henry Capital, LLC, a Delaware limited liability company (“Cape Henry Capital”). By accessing this site and any pages thereof, you agree to be bound by our terms of use and privacy policy. The use of this website does not constitute an application for a mortgage loan or an offer by Cape Henry Capital to lend.

Cape Henry Capital is a mortgage broker and not a lender. Cape Henry Capital is licensed in FL,GA,PA,SC,TX. Please visit www.nmlsconsumeraccess.org for more licensing information.

Mortgage loan products referenced in this website are offered to qualified borrowers for business or commercial purposes only and may be secured by non-owner-occupied properties only.

Origination fees and other fees may apply. Financing is subject to certain restrictions and requirements including, but not limited to, due diligence, credit evaluation, and approval of the subject property. To qualify, borrowers must meet underwriting requirements. Not all borrowers will qualify and not all borrowers that qualify will receive the lowest rate. The actual loan rate and terms depend on a variety of factors. Actual rates, terms, and conditions are subject to change from time to time without notice.

Cape Henry Capital’s principal business address is 500 Studio Drive, Suite 101, Virginia Beach, VA 23452

1340 N. Great Neck Road, Suite 1272, #191 Virginia Beach, VA 23454

Check Out our Newsletter for Market Trends, Updates and Investor Resources