Rental Property Cash-Out Refi: Rules, Math & Strategy

Break the equity trap with a rental property cash-out refi. Learn 2026 rules, LTV and seasoning limits, DSCR math, tax lines, and smart refinance strategies.

DSCR LOANS

Nick Thomas

6/21/20268 min read

Most landlords are sitting on a problem that looks like a success. Their properties have appreciated, their equity has grown, and yet the capital they need to fund the next deal is locked inside the walls of an asset they can't spend. You own the wealth, but you can't use it without selling. That's the equity trap, and a cash out refi on an investment property is how you break out of it.

The mechanics are straightforward: you refinance your existing mortgage into a larger loan, and the difference between the new balance and the old one hits your bank account as cash. No sale. No capital gains event. Just your own equity, unlocked and ready to work again. The catch is that many banks and agency lenders emphasize borrower income and overlays that can be restrictive for investors, even when the property cash flow would otherwise support the loan.

This guide covers what the 2026 rules actually look like for investment-property cash-out refis, how to run the numbers before you apply, where the tax deductibility lines are, and how a DSCR loan from a lender like Cape Henry Capital cuts through the conventional lending maze without requiring you to prove your income on paper.

Cash Out Refi Investment Property: How the Mechanics Actually Work

What the lender is really evaluating

When you do a cash-out refinance, the lender pays off your existing mortgage in full and issues a new, larger loan in its place. You receive the difference as a lump-sum cash payment at closing. This is fundamentally different from a rate-and-term refinance, where the goal is simply to change your interest rate or repayment schedule without extracting equity.

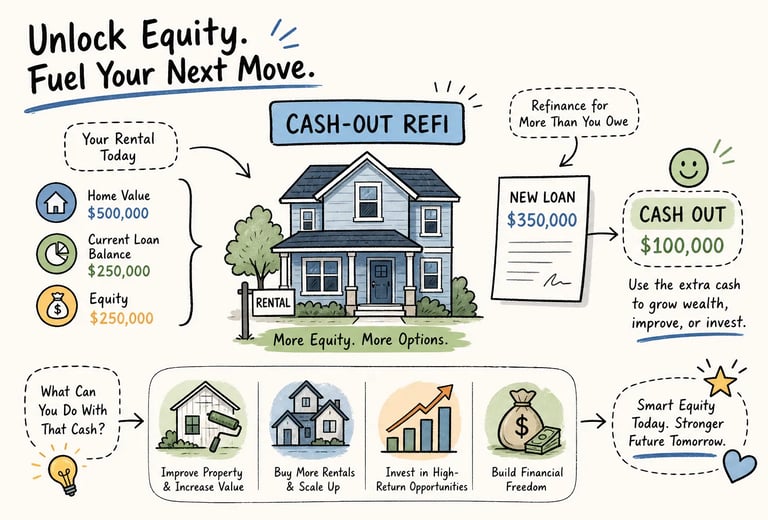

The math is straightforward. Take a property worth $500,000 with an existing loan balance of $300,000. At the standard 75% LTV cap for investment-property cash-out refis, the maximum new loan is $375,000. Subtract the $300,000 payoff, and you have $75,000 in net proceeds before closing costs. That's the equity you've built, now available as deployable capital without selling the asset.

2026 LTV limits and seasoning rules by loan type

Fannie Mae caps investment-property cash-out refinances at 75% LTV and requires that the existing first mortgage be at least 12 months old. At least one borrower must also have been on title for 6 months before the transaction closes. Freddie Mac follows a nearly identical structure, with 12-month first-lien seasoning and 6-month title seasoning required, with LTV limits referenced to the program guide. Major banks typically align with these caps, landing at 75% to 80% LTV with their own overlays on credit score, income documentation, and property condition.

The 12-month seasoning rule is a real obstacle for BRRRR investors who acquire, renovate, and want to pull equity quickly. Agency guidelines simply don't accommodate that timeline. Many DSCR portfolio lenders operate under more flexible rules: most require 6 months of seasoning, some accept 3 months, and certain programs have no seasoning requirement at all for qualifying borrowers. That flexibility is one of the most practical reasons investors move away from agency financing as their portfolios grow.

Why DSCR Loans Are the Investor's Path to Pulling Equity

Qualifying on the property, not your paycheck

DSCR underwriting is built around a single question: does this property generate enough rental income to cover its debt service? The ratio itself is simple. Divide the monthly gross rent by the total monthly mortgage payment. A DSCR of 1.0 means the property breaks even; anything above that means it covers its own debt with income left over. Most private lenders require a minimum DSCR of 1.0 for cash-out refinance approval, with some pushing to 1.1 or 1.25 to unlock better rates and higher LTVs, depending on program and LTV tier.

What DSCR underwriting removes from the equation is your personal income. Self-employed investors, business owners with complex tax returns, and anyone whose W-2 income doesn't reflect their actual financial position can still qualify based entirely on what the property earns. That's a structural shift from how conventional lenders think about risk, and it opens the door for a large portion of active real estate investors who get turned away by banks.

Cape Henry Capital structures DSCR cash-out refinances based on property cash flow, not personal income verification. If you've been sitting on equity and waiting for the right lender, the prequal process is fast and straightforward, and you can request a no-obligation loan evaluation to understand your rate and terms before committing to anything.

How a private DSCR lender structures the deal differently

Working with a portfolio lender like Cape Henry Capital means you're dealing directly with the decision-makers. There's no agency approval layer, no committee review, and no middlemen slowing the process down. Portfolio lenders can move significantly faster than traditional bank timelines, and many offer competitive rate lock periods to protect you while the appraisal completes.

For investors using the BRRRR strategy or actively scaling a portfolio, this speed matters. Equity recycling only works if you can access the capital and redeploy it before the next deal closes. A process that drags for weeks at a bank compresses to a timeline that actually fits how active investors operate.

The Real Numbers: Cash Flow and ROI Impact

Sample calculation on a $500k rental property

Start with the baseline: a $500,000 property, existing loan of $300,000 at 5%, monthly payment of $1,610, and rent at $3,500 per month. Annual operating expenses (taxes, insurance, maintenance) run $12,000. NOI before the refi is $30,000 per year. Cash flow after the mortgage payment is $10,680 annually.

After the cash-out refi: the new loan is $375,000 at 5.5%, bringing the monthly payment to $2,124, a jump of $514 per month. The $75,000 in proceeds funds a renovation that pushes rent from $3,500 to $4,000 per month. NOI rises to $36,000 per year, a 20% increase. Annual cash flow after the new payment lands at $10,512, only $168 less than before the refi. The investor extracted $75,000 in equity and gave up less than $200 in annual cash flow to do it.

The ROI on the deployed capital is 8% pre-tax: a $6,000 increase in annual NOI on $75,000 extracted. If those proceeds fund a down payment on a second property that generates $12,000 in annual cash flow, the return on that equity is significantly higher. The cap rate picture also improves: NOI rising from $30,000 to $36,000 on the same $500,000 value pushes the cap rate from 6.0% to 7.2%.

When the math works and when it doesn't

The numbers work when the rent increase from renovations exceeds the payment increase, or when the extracted capital goes into a second property that generates new income. They fail when the proceeds go toward personal expenses, when rates on the new loan are significantly higher than the existing loan, or when the property can't support a higher rent at all.

One hard rule to keep in mind: interest on cash-out proceeds used for personal expenses is not deductible. Interest on proceeds used for rental improvements or investment property acquisition generally is. That distinction has real tax consequences, and mixing uses creates documentation headaches the IRS will notice.

Tax Rules for the Proceeds: Where the Deductions Follow the Money

Cash-out refinance proceeds are not taxable income. The IRS treats loan proceeds as debt, not earnings, so the disbursement itself creates no tax event. What the IRS does track is how you use the money, because that determines what interest is deductible.

Proceeds directed toward renovating the property that secures the loan generally produce deductible interest as a rental expense on Schedule E. Proceeds used to purchase another investment property typically generate deductible investment interest tied to that acquisition. Use the money for personal expenses, and the interest on that portion is not deductible. Consult IRS guidance or a qualified CPA for the tax implications of a cash-out refinance that applies to your specific situation.

If you split proceeds across multiple uses, the IRS applies tracing rules. The allocation follows the money: 60% to a renovation and 40% to a down payment on a second rental means the refinance interest is deducted at those proportions across each use category. Clean documentation of exactly where the cash went is not optional; it's the foundation of your deduction. For mixed-use scenarios, work with a CPA before and after closing, not after an audit letter arrives.

Cash Out Refi Investment Property: Portfolio Lenders vs. Agency Loans

Agency loans run on standardized income documentation. Cash-out refinance rental property guidelines from industry sources generally reflect those agency constraints: Fannie Mae and Freddie Mac guidelines require consistent income verification, and their reserve requirements for investment-property cash-out typically land at 6 months of PITIA across every financed property in the portfolio. For an investor with five properties, that's a significant amount of capital that has to sit liquid before the lender will approve the deal.

Many DSCR portfolio lenders operate differently across nearly every dimension that matters to active investors:

Income documentation: many DSCR programs accept bank statements, asset depletion, or property cash flow in lieu of W-2s or tax returns; documentation requirements vary by lender and program

DTI limits: higher thresholds accepted with compensating factors like reserves or strong DSCR

Reserves: typically 2 months of PITIA on the subject property only, not across the entire portfolio; cash-out proceeds can often count toward reserve requirements

Seasoning: 3 to 6 months for most programs versus the 12-month agency requirement

The tradeoff is real: portfolio lenders price slightly higher in rate and sometimes in fees than agency loans. For most investment-property cash-out refis in 2026, rates have generally ranged from 7.0% to 7.5% depending on LTV, credit score, and property type, running roughly 0.5% to 1.0% above primary-home cash-out pricing. Closing costs typically land between 2% and 5% of the new loan amount and can often be rolled into the loan balance. That premium is the cost of flexibility, and for investors who can't or won't qualify through agency channels, it's not a choice at all.

What to Organize Before Your First Call

Documents to gather before you apply

Getting your file organized before the first call shortens the timeline and removes friction from the approval process. Gather your current mortgage statement and payoff balance, all current lease agreements, and 12 months of rental deposit history. Pull your most recent appraisal or a current property value estimate, along with property tax and insurance statements. If the property is held in an LLC, have your entity documents ready.

Steps from first contact to funded loan

Run the LTV math first. Estimate your property value, subtract the 75% LTV cap, then subtract the existing balance to see your rough cash-out ceiling.

Get prequalified. With Cape Henry Capital, the prequal process is fast and generates a letter you can use to move quickly on your next step.

Submit for a no-obligation quote. Loan evaluations come back quickly, so you know your rate and terms before committing to anything.

Order the appraisal and lock your rate. Cape Henry Capital offers competitive rate lock periods, so you're protected while the appraisal completes.

Clear underwriting conditions and schedule closing. With direct underwriter access and no agency approval layer, this stage moves faster than a traditional bank process by a significant margin.

Put Your Equity to Work

A cash out refi on an investment property is one of the most capital-efficient tools available to active investors. You don't sell the asset. You don't trigger a tax event on the extraction. You pull the equity your property has earned and put it back to work, funding renovations that increase NOI, acquiring the next property, or accelerating a BRRRR cycle that builds long-term wealth without starting from zero each time. Learn more about how a typical bank explains cash-out refinance basics on PNC's cash-out refinance page.

The conventional lending path makes this harder than it needs to be, especially for investors without clean W-2 income. DSCR underwriting solves that by focusing on what actually matters: what the property earns and whether it can service the new debt.

Cape Henry Capital is built for exactly this scenario. DSCR cash-out refis that qualify on property cash flow, not personal income verification, with direct access to the underwriters making the decisions. Run your numbers first with the free DSCR Loan Calculator on the Cape Henry Capital website, then request a no-obligation quote. Your equity has been sitting as an unrealized gain long enough. It's time to put it to work as capital.

Tailored loans for real estate investors.

info@capehenrycapital.com

p. 757-267-9495

© Cape Henry Capital, LLC. 2023 All Rights Reserved. NMLS # 2383447.

Capehenrycapital.com is a website operated Cape Henry Capital, LLC, a Delaware limited liability company (“Cape Henry Capital”). By accessing this site and any pages thereof, you agree to be bound by our terms of use and privacy policy. The use of this website does not constitute an application for a mortgage loan or an offer by Cape Henry Capital to lend.

Cape Henry Capital is a mortgage broker and not a lender. Cape Henry Capital is licensed in FL,GA,PA,SC,TX. Please visit www.nmlsconsumeraccess.org for more licensing information.

Mortgage loan products referenced in this website are offered to qualified borrowers for business or commercial purposes only and may be secured by non-owner-occupied properties only.

Origination fees and other fees may apply. Financing is subject to certain restrictions and requirements including, but not limited to, due diligence, credit evaluation, and approval of the subject property. To qualify, borrowers must meet underwriting requirements. Not all borrowers will qualify and not all borrowers that qualify will receive the lowest rate. The actual loan rate and terms depend on a variety of factors. Actual rates, terms, and conditions are subject to change from time to time without notice.

Cape Henry Capital’s principal business address is 500 Studio Drive, Suite 101, Virginia Beach, VA 23452

1340 N. Great Neck Road, Suite 1272, #191 Virginia Beach, VA 23454

Check Out our Newsletter for Market Trends, Updates and Investor Resources