Fix-and-Flip Loans: Rates, Leverage, and How to Qualify

Fix-and-flip profits aren’t made at the closing table — they’re made when you structure the financing correctly from day one. This guide breaks down today’s fix-and-flip loan rates, leverage limits, approval requirements, and deal math so investors can fund smarter, close faster, and protect their ROI before making an offer.

FIX & FLIP LOANS

Nick Thomas

5/25/20269 min read

Every flip lives or dies on the spread between what you pay and what you sell for. Most investors obsess over the purchase price and the after-repair value, but the line item that quietly kills margins sits in between: financing cost. A loan structured the wrong way, at the wrong rate, with the wrong timeline, doesn't just thin your profit; it can erase it entirely. Fix-and-flip loans, sometimes searched as a fix flip loan, exist specifically to solve this problem. They're not a generic mortgage repurposed for investors; they're a purpose-built product designed around how flips actually work.

At Cape Henry Capital, we structure these deals daily for investors ranging from first-time flippers to operators running 20-plus projects a year. The mechanics, the costs, and the qualification math are the same whether you're doing one flip or ten. What changes is how well-prepared you are before you apply. This guide gives you everything you need to evaluate financing costs, understand leverage limits, qualify confidently, and model your deal before you make an offer.

What a fix-and-flip loan actually is (and how it works)

A fix-and-flip loan is a short-term, asset-based loan that funds two things at once: the property acquisition and the renovation budget. Unlike a conventional mortgage, approval is based primarily on the deal itself, specifically the property's after-repair value (ARV) and the overall project cost, rather than your W-2 income or debt-to-income ratio. The lender is betting on the asset, not your personal income statement.

The mechanics work like this: at closing, the lender funds the purchase. The rehab budget is held in reserve and released in stages, called draws, as work is completed and inspected. Each draw is tied to a milestone in the construction scope. This structure protects the lender's collateral position and keeps the investor disciplined about rehab progress. It also means you're only paying interest on the drawn balance, not the full loan amount, from day one.

How purchase and rehab funding are packaged together

The acquisition funds and the rehab holdback are structured as a single loan instrument, not two separate products. At closing, the purchase portion funds. The rehabilitation reserve sits with the lender until you submit draw requests, which are typically supported by inspection reports or contractor invoices. This bundled approach simplifies your capital stack and eliminates the need to line up separate renovation financing after the purchase closes.

Loan terms: duration, repayment structure, and exit

Most fix-and-flip loans run 6 to 18 months, with interest-only payments during the hold period. You're not amortizing principal while the property is under renovation, which keeps monthly carrying costs manageable. When the project is complete, you exit the loan either by selling the property and repaying the balance from proceeds, or by refinancing into a long-term DSCR rental loan if you decide to hold. Lenders will ask about your exit strategy at application, so have a clear answer before you sit down with them.

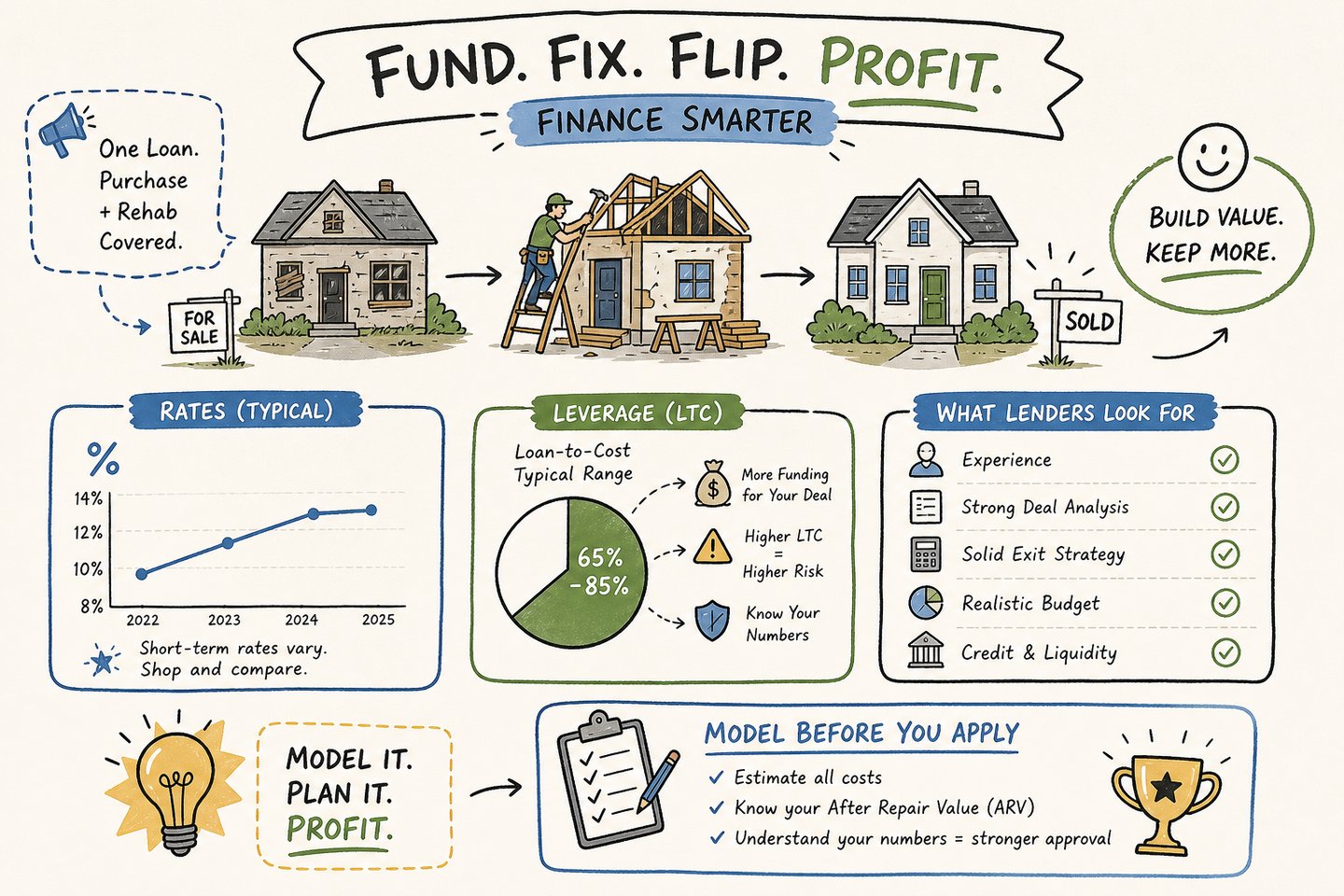

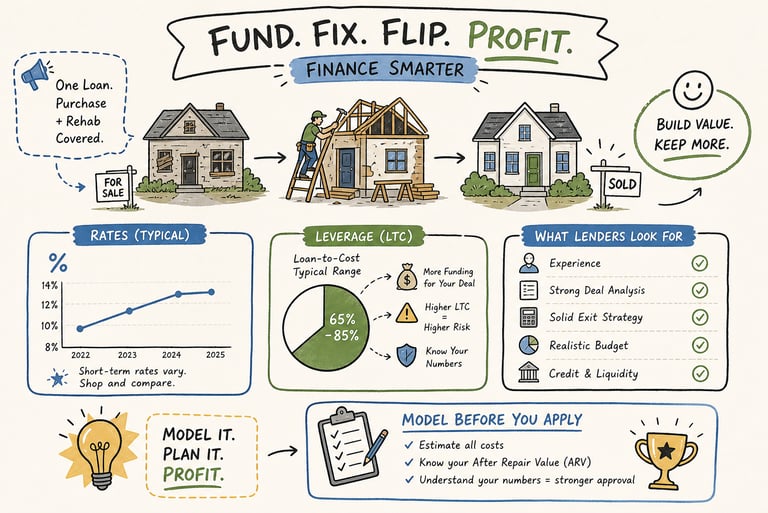

Current rates, points, and what financing actually costs your flip

Fix-and-flip loan rates in 2025, 2026 range from 9% to 12% for most private lenders, with averages clustering around 10.4% to 11% based on deals we're seeing in the current market. Experienced investors with strong credit profiles can access rates from 8.5% to 10.5%, while newer borrowers or those with thinner credit histories typically land in the 11% to 13% range. These rates reflect the short-term, asset-based nature of the product, not a penalty for being an investor. For more market context, we update our rates regularly for investors.

The interest rate is only part of your financing cost. Origination fees run 1% to 3% of the loan amount, processing fees add $1,000 to $2,000 at closing, and legal costs average around $1,900. On a $300,000 loan, a 2% origination fee adds $6,000 upfront. Carry that loan for six months at 11%, and you're looking at $16,500 in interest on top of the origination costs. That's a total financing cost of roughly $24,400 on a $300,000 project before you account for any other expenses. That number belongs in your pro forma before you make an offer, not after.

Points, fees, and what shows up at closing

Origination fees are negotiable, especially for experienced borrowers with clean documentation. Experience matters here too. Investors who show up with a strong track record and a well-supported ARV position themselves to negotiate terms more effectively than those who submit disorganized applications. Every fee line is controllable. The best way to reduce your cost of capital is to be an organized, credentialed borrower, not just a borrower with a great deal.

Interest rate ranges by borrower profile

Credit score and deal experience are the two biggest rate drivers. Borrowers with 740-plus credit scores and a documented history of multiple completed flips access the lower end of the rate range. First-time investors or those with credit in the 620, 680 range should budget for rates toward the higher end. The spread between best-case and worst-case rates on the same deal can be 2% to 3%, which over a six-month hold on a $300K loan represents $3,000 to $4,500 in additional carrying cost. That's real money.

Leverage limits: how LTC and ARV determine what you can borrow

Two ratios govern how much you can borrow on a fix-and-flip: loan-to-cost (LTC) and loan-to-after-repair-value (LTARV). LTC measures the loan amount against your total project cost, which is the purchase price plus the full rehab budget. LTARV caps the loan at a percentage of what the property will be worth after renovation is complete, typically 70% to 75%. Both ratios apply, and whichever produces the lower number sets your borrowing limit.

Consider a concrete example: a property priced at $150,000 with $50,000 in rehab costs and an ARV of $280,000 has a total project cost of $200,000. At 90% LTC, the lender would fund up to $180,000. At 75% LTARV, the cap is $210,000. In this scenario, the LTC limit binds first, meaning your maximum loan is $180,000, and you need to bring $20,000 to the table in addition to your costs. Run both calculations on every deal before you apply.

What top lenders actually offer on LTC

Experienced investors with two or more completed flips can access 90% to 95% LTC, with some lenders covering 100% of rehab costs through the draw structure. First-time flippers typically see 75% to 85% LTC, with adjusted terms to compensate for the execution risk. The principle is simple: experience is leverage. Every flip you document adds to your credibility and directly increases the capital you can access on the next deal.

Why ARV is the number that really runs the deal

The ARV cap exists because lenders need a buffer if the market shifts or the renovation runs over. Investors who understand their comp set and can substantiate their ARV with real, recent data close faster and borrow more than those who rely on optimistic assumptions. Your comp package, the three to five sold properties that support your projected value, is not a formality. It's a direct input into your borrowing capacity. Pull it early, pull it carefully, and present it clearly.

What fix-and-flip lenders look for before they fund your deal

Approval for a fix-and-flip loan rests on three things: deal quality, borrower readiness, and exit strategy clarity. Most private lenders require a minimum credit score of 620 to 680, but credit is rarely the deciding factor. A deal with strong comps, a realistic rehab budget, and an investor who has done this before will get funded at favorable terms even if the credit profile isn't perfect. Conversely, excellent credit paired with a weak deal doesn't change the lender's math.

Credit, experience, and how lenders weight each

Two or more completed flips typically unlocks the highest LTC tiers across most private lenders. If you're on your first deal, document everything you have: relevant construction background, your team's credentials, and any adjacent real estate experience. First-time investors aren't automatically disqualified; they just face more conservative terms. Bridge that gap with preparation, not promises.

The documentation package that moves a deal forward fast

The items every lender needs at application are consistent across the market. Have these ready before you submit:

Signed purchase contract

Itemized rehab budget and signed contractor bid

Two to six months of bank statements

Proof of reserves covering 15% to 25% of total project cost

Three to five ARV comps

LLC entity documents if taking title in a business entity

Incomplete documentation is the single biggest cause of delayed closings. It's rarely a lender speed problem; it's almost always a borrower preparation problem. Submit everything at once, in a clear format, and closings move fast.

How fast approval and closing actually happen

Private and hard money lenders can approve a deal in 24 to 48 hours and close in 7 to 10 days when the documentation package is complete. Traditional banks take 45 to 60 days and often won't touch distressed properties at all. In competitive markets where deals move in hours, that timing gap isn't a minor inconvenience. It's the difference between winning the contract and watching another investor close it. For additional context on typical timelines and underwriting requirements, read more about underwriting requirement for bridge loans.

Fix-and-flip loans vs. your other financing options

HELOCs, cash, bridge loans, and FHA 203k loans each have their place, but none of them are purpose-built for the purchase-plus-rehab workflow that defines a flip. Understanding the differences helps you confirm you're using the right tool, not just the most familiar one. If you want to compare if Fix-and-Flip or other bridge loan options, sign-up for a free consulation.

When hard money and bridge loans overlap with fix-and-flip financing

Bridge loans and hard money loans are often used interchangeably with fix-and-flip financing, and the overlap is real. Bridge loans are broader in scope, covering property transitions, rental acquisitions, and flips. Hard money is asset-based and speed-focused but doesn't always include a structured rehab draw. A dedicated fix-and-flip loan specifically combines purchase financing with milestone-based rehab disbursements into a single product. For active flippers, the draw structure is what separates this type of short-term investor loan from generic bridge or hard money financing.

Why HELOCs and FHA 203k fall short for active flippers

HELOCs offer lower rates, typically around 7% variable, but they require existing equity in another property, carry variable rate risk, and have no built-in rehab draw structure. They can work for a single, small-scale flip if you already own equity-rich real estate, but they don't scale. FHA 203k loans require owner-occupancy, which eliminates them as a flip tool entirely. They also run on conventional bank timelines of 30-plus days with extensive appraisal and inspection requirements. For investors doing multiple flips a year, neither product is a realistic operational tool.

Structuring your flip financing to protect ROI before you apply

The single most common mistake active flippers make is calculating deal profitability after they're under contract. By then, financing terms are partially locked, the clock is running, and there's no room to renegotiate the purchase price based on what the loan actually costs. Running deal math before you make an offer isn't overly cautious; it's how experienced investors stay profitable across a portfolio.

Model the deal before you bid (and before you apply)

A complete pre-offer model includes the purchase price, full rehab budget, projected ARV, financing cost at a realistic rate including origination fees, estimated hold time, selling costs, and projected net margin. Cape Henry Capital's free Turn-Key Deal Calculator is built for exactly this workflow. Plug in your numbers, loan amount, rate, and rehab budget, and see your real margin before you commit any capital. No application required, no conversation needed. Run the scenario in minutes and know whether the deal works before you bid.

The lender checklist that shortens your closing timeline

Speed at closing is almost always a function of borrower readiness, not lender capacity. Investors who close in 7 days show up with complete documentation, pre-arranged contractor bids, comps pulled in advance, clearly documented reserves, and an LLC entity ready to take title. Investors who wait 30 days are usually waiting on their own paperwork. The preparation you do before application is what determines how fast you get funded, not which lender you call.

Know your numbers before you make your move

Once you understand the inputs, evaluating a fix flip loan becomes a repeatable process. Rates run 9% to 12% for most private lenders in the current market. The ARV cap sits at 70% to 75%, and experienced investors can access 90% to 95% LTC with 100% rehab coverage. With complete documentation, a well-supported deal can get approved and funded in 7 to 10 days. Every one of those numbers belongs in your deal model before you make an offer.

If you're ready to run a specific deal scenario, start with Cape Henry Capital's free Turn-Key Deal Calculator. Navigate to the bridge loan calculator page and select Fix and Flip. Enter your purchase price, rehab budget, loan amount, and estimated carry cost to see your real margin before you sit down with a lender. When you're ready to move on a deal, you can get a no-obligation loan quote within 24 hours and a prequalification letter in under 10 minutes. The deal is out there. Don't let financing be the reason it slips.

Tailored loans for real estate investors.

info@capehenrycapital.com

p. 757-267-9495

© Cape Henry Capital, LLC. 2023 All Rights Reserved. NMLS # 2383447.

Capehenrycapital.com is a website operated Cape Henry Capital, LLC, a Delaware limited liability company (“Cape Henry Capital”). By accessing this site and any pages thereof, you agree to be bound by our terms of use and privacy policy. The use of this website does not constitute an application for a mortgage loan or an offer by Cape Henry Capital to lend.

Cape Henry Capital is a mortgage broker and not a lender. Cape Henry Capital is licensed in FL,GA,PA,SC,TX. Please visit www.nmlsconsumeraccess.org for more licensing information.

Mortgage loan products referenced in this website are offered to qualified borrowers for business or commercial purposes only and may be secured by non-owner-occupied properties only.

Origination fees and other fees may apply. Financing is subject to certain restrictions and requirements including, but not limited to, due diligence, credit evaluation, and approval of the subject property. To qualify, borrowers must meet underwriting requirements. Not all borrowers will qualify and not all borrowers that qualify will receive the lowest rate. The actual loan rate and terms depend on a variety of factors. Actual rates, terms, and conditions are subject to change from time to time without notice.

Cape Henry Capital’s principal business address is 500 Studio Drive, Suite 101, Virginia Beach, VA 23452

1340 N. Great Neck Road, Suite 1272, #191 Virginia Beach, VA 23454

Check Out our Newsletter for Market Trends, Updates and Investor Resources