Best DSCR Loan Calculator: Simplify Your Loan Decisions Today

A DSCR loan calculator helps you determine if your property’s income can cover its debt obligations. By inputting key financial details like your property’s purchase price, rental income, and expenses, you can quickly see if you meet lenders’ criteria. In this article, we’ll guide you on how to use a DSCR loan calculator effectively. The DSCR loan calculator can also help estimate the maximum loan amount based on the property's income and expenses.

DSCR LOANS

3/24/202510 min read

Best DSCR Loan Calculator: Simplify Your Loan Decisions Today

A DSCR loan calculator helps you determine if your property’s income can cover its debt obligations. By inputting key financial details like your property’s purchase price, rental income, and expenses, you can quickly see if you meet lenders’ criteria. In this article, we’ll guide you on how to use a DSCR loan calculator effectively. The DSCR loan calculator can also help estimate the maximum loan amount based on the property's income and expenses.

Key Takeaways

The Debt Service Coverage Ratio (DSCR) is essential for investors and lenders, determining a property’s income generation ability against its debt obligations, with values above 1 indicating positive cash flow.

Using a DSCR loan calculator streamlines the assessment of loan eligibility by requiring specific inputs like property purchase price, interest rate, rental income, and expenses for accurate calculations.

A good DSCR is typically considered to be 1.25 or higher, and improving this ratio can enhance loan terms, eligibility, and overall financial stability for real estate investments.

Understanding DSCR and Its Importance

The Debt Service Coverage Ratio (DSCR) is a crucial financial metric that stands for Debt Service Coverage Ratio. Calculated by dividing the net operating income by the total debt service, the DSCR provides a clear picture of a property’s income generation potential against its debt obligations. This ratio is vital for both investors and lenders, as it helps determine profitability for the former and repayment ability for the latter.

For real estate investors, calculating the DSCR directly impacts loan eligibility. Properties with a DSCR below 1.0 are often considered high-risk since they generate insufficient income to meet debt servicing requirements. On the other hand, a DSCR value above 1.2 indicates that the property’s income is sufficiently covering its debt, making it more attractive to lenders. A higher DSCR can also help in determining the maximum loan amount a real estate investor can qualify for.

Lenders typically require a minimum DSCR between 1.0 and 1.5, depending on the property type and market conditions. This threshold ensures sufficient income to cover debt obligations. A DSCR value greater than 1 indicates positive cash flow, covering mortgage payments and reflecting financial health.

A higher DSCR improves loan approval chances and ensures your investment generates enough income to cover its debts, making DSCR indispensable for real estate investors.

Definition of DSCR

The Debt Service Coverage Ratio (DSCR) is a financial calculation used to assess a borrower’s ability to repay a loan by comparing their net operating income (NOI) to their total debt service. This ratio is crucial for lenders as it helps evaluate the creditworthiness of real estate investors and the likelihood of loan repayment. A DSCR of 1 or higher indicates that the borrower’s NOI is sufficient to cover their debt obligations, suggesting a lower risk of default. Conversely, a DSCR below 1 implies that the borrower may struggle to meet their loan payments, signaling potential financial instability.

DSCR Formula: Net Operating Income / Total Debt Service

The DSCR formula is straightforward yet powerful, calculated by dividing the borrower’s net operating income (NOI) by their total debt service. The formula is as follows:

DSCR = NOI / Total Debt Service

Where:

NOI (Net Operating Income): This is the gross income generated by the property minus operating expenses. It represents the actual earnings from the property before debt obligations are considered.

Total Debt Service: This includes all debt obligations, such as loan payments, interest, and principal. It reflects the total amount required to service the debt on the property.

By using this formula, real estate investors and lenders can quickly determine whether a property generates enough income to cover its debt obligations, aiding in loan approval decisions.

How DSCR Loans Work

DSCR loans are a specialized financing option designed specifically for real estate investors. Unlike traditional loans that rely on the borrower’s personal income for qualification, DSCR loans use the property’s income to determine eligibility. This approach allows investors to leverage the cash flow generated by their investment properties, such as rental units or commercial buildings, to secure financing.

These loans are particularly beneficial for real estate investors looking to expand their portfolios without being constrained by their personal income levels. By focusing on the property’s income, DSCR loans provide a more accurate assessment of the investment’s financial viability, making them an attractive option for both novice and experienced investors.

What is a DSCR Loan?

A DSCR loan is a type of rental property loan that uses the debt service coverage ratio to evaluate the real estate investors ability to repay the loan. These loans are typically utilized by real estate investors who aim to purchase or refinance investment properties. DSCR loans are ideal for financing properties that generate rental income, such as apartment buildings, commercial properties, or other income-producing real estate.

By relying on the property’s income rather than the borrower’s personal income, DSCR loans offer a flexible and efficient financing solution. This makes them particularly appealing to investors seeking to maximize their investment potential while minimizing the documentation and income verification typically required by traditional loans.

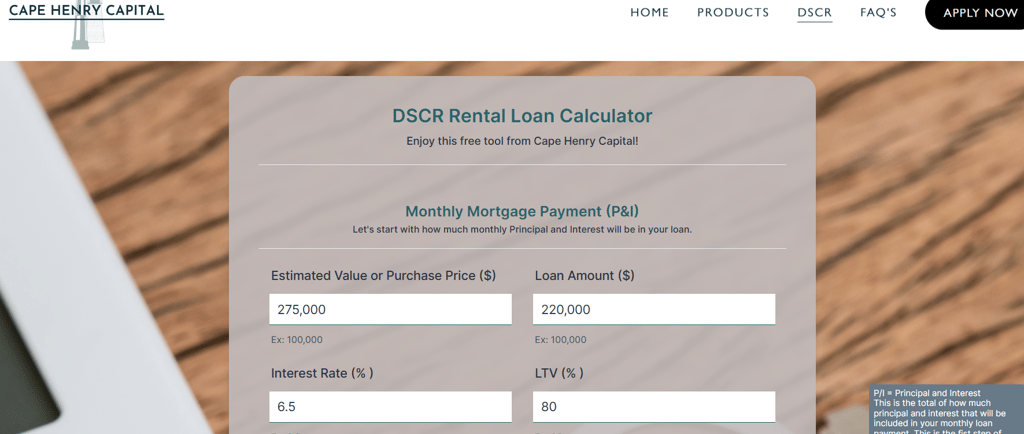

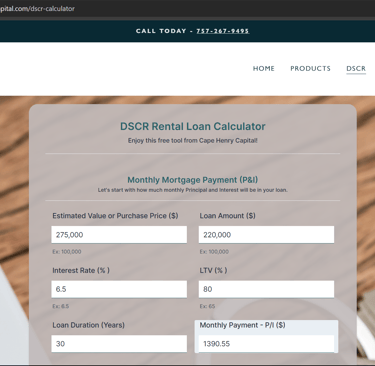

How to Use Our DSCR Loan Calculator

Our DSCR calculator simplifies determining your debt service coverage ratio, helping you quickly assess loan qualification. You’ll need to provide financial data like the property’s purchase price, down payment, interest rate, and other expenses. Accurate DSCR calculation depends on the quality of input data, such as net operating income and debt payments. The DSCR calculator can also help estimate the maximum loan amount based on the provided financial data.

Start by entering the purchase price of the property, specifying the interest rate and loan term. Then, provide the total monthly rental income and your monthly expenses and mortgage debt obligations.

Let’s break down each step in detail to ensure you get the most accurate results.

Input Property's Purchase Price

The first step in using the DSCR calculator is to input the property’s purchase price. This figure is crucial as it sets the foundation for your loan calculation. For example, Jenny is considering a rental property with a purchase price of $200,000. By entering this amount into the calculator, she can begin to assess whether the property qualifies for a DSCR loan.

The lender will then use this information to determine the total loan amount based on the Debt Service Coverage Ratio.

Specify Interest Rate and Loan Term

Next, you’ll need to specify the interest rate and loan term. Inputting the current interest rate is essential for accurate monthly payment calculations. Interest rates can vary, so it’s crucial to use the most up-to-date rate available.

The loan term, which typically ranges from 5 to 25 years for DSCR loans, also plays a significant role in determining your loan payments. Longer loan terms generally result in lower monthly payments, which can positively impact your DSCR.

Accurate input of the interest rate and loan payment term is crucial for precise monthly payment calculations.

Provide Total Monthly Rental Income

Next, provide the total monthly rental income, representing the gross income your property generates each month. Accurate gross rental income data is essential for calculating monthly net operating income, impacting overall investment evaluation. For instance, if your property generates $3,000 in monthly rent, enter this figure into the calculator to determine its impact on your DSCR.

Precise gross rental income data allows investors to make informed financial decisions, ensuring the DSCR calculation reflects the true income potential of the property.

Enter Monthly Expenses and Debt Obligations

Finally, enter your monthly expenses and debt obligations, including operating costs such as property insurance, maintenance, and utilities. Accurate documentation of these expenses is crucial for the DSCR calculation.

Consider the vacancy rate, calculated as (Number of Days Vacant) / (Number of Days Available for Rent). Entering all relevant expenses and debt obligations ensures an accurate DSCR calculation, providing a true assessment of your property’s financial health.

Interpreting Your DSCR Result

After inputting all necessary data into the DSCR calculator, interpreting the result is crucial. A DSCR exceeding 1 indicates your property can comfortably cover its debt expenses with its earnings. Lenders generally prefer higher DSCR values, signaling a lower risk of default.

If your DSCR is under 1, it suggests that the property does not generate enough income to meet its debt obligations, indicating a cash flow negative situation. Properties with a DSCR less than 1.25 may face lower loan value or higher interest rates, making it crucial to aim for a DSCR of at least 1.1 to 1.2 for stability.

Monitoring changes in your DSCR over time offers valuable insights into your evolving financial stability.

What Is a Good DSCR?

A good DSCR is typically considered to be 1.25 or higher. This indicates that the income generated by the property exceeds its debt obligations by 25%, ensuring that the borrower has sufficient income to cover their debt service. Most lending institutions require a DSCR of at least 1.25 to qualify for a loan, reflecting strong financial health and lower risk.

A DSCR above 1.25 can lead to better loan terms, such as reduced interest rates and more favorable repayment conditions. For instance, a DSCR of 1.50 suggests that the property’s income not only meets but exceeds total debt obligations, providing surplus income.

Conversely, a DSCR less than 1 suggests that a borrower may not generate enough income to cover debt obligations, which can lead to disqualification for loans.

Improving Your DSCR

Enhancing your DSCR improves loan eligibility and secures better terms. Boosting net operating income (NOI) by increasing rental income or adjusting to market rates directly improves DSCR, making your investment more attractive to lenders.

Additionally, reducing operating costs and debt obligations can significantly enhance your debt service coverage ratio. Consider refinancing to secure more favorable debt payments or extending the loan term to lower monthly payments. Minimizing new debt and paying down existing loans can also positively affect your DSCR.

Implementing these strategies improves financial metrics and increases loan approval chances.

Benefits of Using a DSCR Calculator

Using a DSCR calculator offers several benefits, expediting the loan application process by simplifying data collection and providing immediate insights into loan eligibility. This tool also aids in budgeting by factoring in all necessary property expenses.

Moreover, the DSCR calculator allows investors to assess multiple financing scenarios and their potential impacts on cash flow. This provides valuable insights into your financing options and investment strategies, helping you make informed decisions.

Maintaining a high DSCR can lead to lower interest rates and favorable repayment conditions.

DSCR Loans: A Tool for Real Estate Investors

DSCR loans are a vital financing option for real estate investors, providing an alternative assessment of their ability to repay loans based on property cash flow rather than personal income. This allows a real estate investor to potentially expand their portfolios without being restricted by traditional income metrics.

These loans enable investors to use rental property cash flow for loan qualification, streamlining the approval process. Available to novice and experienced investors, DSCR loans can be used for multiple properties and typically require less documentation than traditional loans, reducing the burden on borrowers.

Factors Affecting DSCR Loan Rates and Terms

Several factors influence DSCR loan rates and terms. Interest rates for DSCR loans fluctuate with market conditions and borrower profiles, reflecting broader economic trends. Economic elements like interest rates and housing market trends can significantly sway DSCR loan conditions.

The Loan-to-Value (LTV) ratio is crucial, with lenders favoring lower ratios for reduced risk. The debt-to-income (DTI) ratio reflects total debt obligations compared to income, aiding in evaluating repayment capacity. The interest coverage ratio shows a borrower’s ability to pay interest on outstanding debt and is relevant in assessing financial health.

Cash flow margin provides insight into operational efficiency by determining the percentage of revenue exceeding expenses. The borrower’s financial profile, including LTV and DTI, directly influences DSCR loan rates and terms. Private lenders often offer more flexible DSCR loan terms compared to traditional banks.

Other Financial Ratios to Consider

Besides DSCR, understanding other financial ratios provides a comprehensive picture of a property’s financial health for loan applications. A good DSCR is typically 1.25 or higher, indicating a stronger ability to cover debt obligations, which lenders often seek during approvals.

Other important financial ratios to consider include the Loan-to-Value (LTV) ratio and the Internal Rate of Return (IRR), which help assess risk and projected profitability.

Improving DSCR can lead to better loan terms, lower interest rates, and increased chances of approval, benefiting overall investment strategy.

Example Calculation Using Cape Henry Capital's DSCR Calculator

Suppose you have a rental property with a net operating income (NOI) of $5,000 per month and an annual debt service amount of $55,000. Calculate DSCR by dividing gross monthly rental income by monthly debt payments. In this case, monthly debt payments would be approximately $4,583 ($55,000 / 12 months).

Input these figures into the DSCR calculator to find a DSCR of 1.82. This high DSCR indicates the property generates sufficient income to cover its debt obligations comfortably, making it attractive to lenders.

The calculator offers a clear, immediate understanding of your financial standing, aiding in making informed investment decisions.

Next Steps After Calculating DSCR

After calculating your DSCR, interpret the results and plan your strategy. If your DSCR meets or exceeds lenders’ requirements, proceed confidently with your loan application, knowing your property is financially sound. The DSCR calculator also assesses factors like interest rates, rent, taxes, insurance, and HOA fees, providing a comprehensive view of your financial situation.

If your DSCR falls short, consider strategies like increasing rental income or reducing operating expenses. Explore other financing options or consult with financial experts for tailored advice. These steps can enhance your financial metrics and increase your chances of securing favorable loan terms.

Summary

In summary, the Debt Service Coverage Ratio (DSCR) is a critical metric for real estate investors, providing insight into a property’s ability to cover its debt obligations. Using a DSCR calculator simplifies the loan application process, offering immediate insights into loan eligibility and helping you make informed decisions. By understanding and improving your DSCR, you can secure better loan terms and ensure the financial health of your investments. Empower yourself with the knowledge and tools to navigate the complexities of real estate financing confidently.

Frequently Asked Questions

What is the Debt Service Coverage Ratio (DSCR)?

The Debt Service Coverage Ratio (DSCR) is a critical financial indicator that assesses a property’s capacity to meet its debt obligations through net operating income. It is determined by dividing net operating income by total debt service.

What is considered a good DSCR for loan approval?

A good Debt Service Coverage Ratio (DSCR) for loan approval is generally considered to be 1.25 or higher, as it shows that the property's income surpasses its debt obligations by at least 25%, which is a common requirement by lenders.

How can I improve my DSCR?

To improve your Debt Service Coverage Ratio (DSCR), focus on increasing your net operating income by raising rental rates or cutting operating expenses. Consider refinancing or paying down existing debt to reduce monthly payments. These steps will enhance your financial stability and make your investments more viable.

Why should I use a DSCR calculator?

Using a DSCR calculator is essential as it streamlines the loan application process and offers immediate insights into loan eligibility. This tool aids in budgeting and evaluating various financing scenarios, enabling you to make informed investment decisions.

What factors affect DSCR loan rates and terms?

DSCR loan rates and terms are primarily influenced by interest rates, Loan-to-Value (LTV) ratio, debt-to-income (DTI) ratio, and the borrower's financial profile, alongside prevailing market conditions and economic trends. These factors collectively determine the cost and accessibility of such loans.

Tailored loans for real estate investors.

info@capehenrycapital.com

p. 757-267-9495

© Cape Henry Capital, LLC. 2023 All Rights Reserved. NMLS # 2383447.

Capehenrycapital.com is a website operated Cape Henry Capital, LLC, a Delaware limited liability company (“Cape Henry Capital”). By accessing this site and any pages thereof, you agree to be bound by our terms of use and privacy policy. The use of this website does not constitute an application for a mortgage loan or an offer by Cape Henry Capital to lend.

Cape Henry Capital is a mortgage broker and not a lender. Cape Henry Capital is licensed in FL,GA,PA,SC,TX. Please visit www.nmlsconsumeraccess.org for more licensing information.

Mortgage loan products referenced in this website are offered to qualified borrowers for business or commercial purposes only and may be secured by non-owner-occupied properties only.

Origination fees and other fees may apply. Financing is subject to certain restrictions and requirements including, but not limited to, due diligence, credit evaluation, and approval of the subject property. To qualify, borrowers must meet underwriting requirements. Not all borrowers will qualify and not all borrowers that qualify will receive the lowest rate. The actual loan rate and terms depend on a variety of factors. Actual rates, terms, and conditions are subject to change from time to time without notice.

Cape Henry Capital’s principal business address is 500 Studio Drive, Suite 101, Virginia Beach, VA 23452

1340 N. Great Neck Road, Suite 1272, #191 Virginia Beach, VA 23454